18/09/2023

Heterogeneous inflation creating difficulties

Newsletter #62 - September 2023

HICP in the EU is not one number!

Many commentators on inflation are very quick to focus on one number or the trend of part of the HICP (Harmonized Index of Consumer Prices) inflation.

Very often, the headlines talk about one specific part of the overall picture regarding inflation and conveniently ignore all other aspects of the inflation puzzle.

Fortunately, the ECB does take all aspects of the inflation picture into account when determining the direction of monetary policy.

As the ECB and other central banks are not oracles with perfect foresight, they can get monetary policy wrong, as they did after COVID-19. Today, they are living with the consequences of those mistakes.

The fundamental problem for the ECB’s Governing Council, its monetary decision-makers, is clearly illustrated in Figure 1.

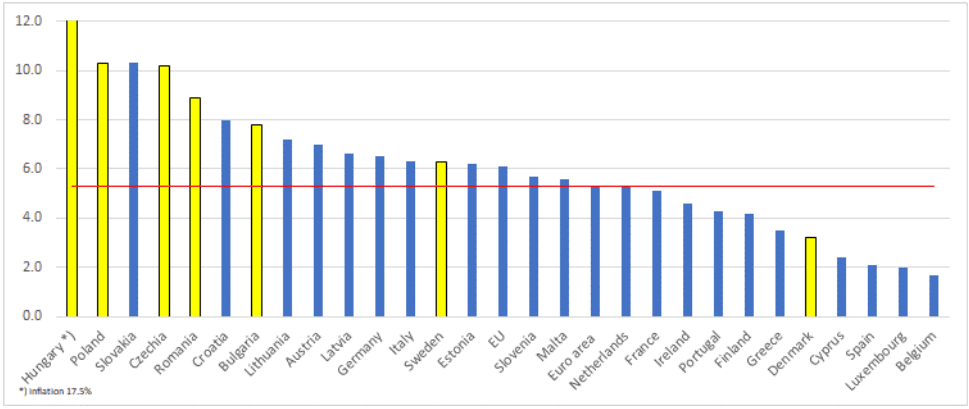

Figure 1 HICP inflation July 2023 source Eurostat

The inflation picture is not the same all over the EU, not even in the eurozone.

While non-eurozone countries (in yellow, above) have independent monetary policies, they are of course closely linked to the ECB’s decisions.

The weighted HICP inflation in the eurozone was 5.3% in July 2023, but that ranges between Slovakia, with more than 10% inflation, to Luxembourg at 2% and Belgium with less than 2%. The largest economy with the highest weight in the index, Germany, has inflation above 6%, while France (the second largest) is slightly under 5.3%.

Clearly, one size does not fit all!

For the ECB, one thing is clear: 5.3% is nowhere near its target of 2% inflation.

But without food and energy!

Many economists like to look at core inflation, which is the HICP excluding the volatile subindex for food and energy. Core inflation is traditionally a more rigid, less volatile index. However, one should not forget that core inflation rigidity works both ways – up and down.

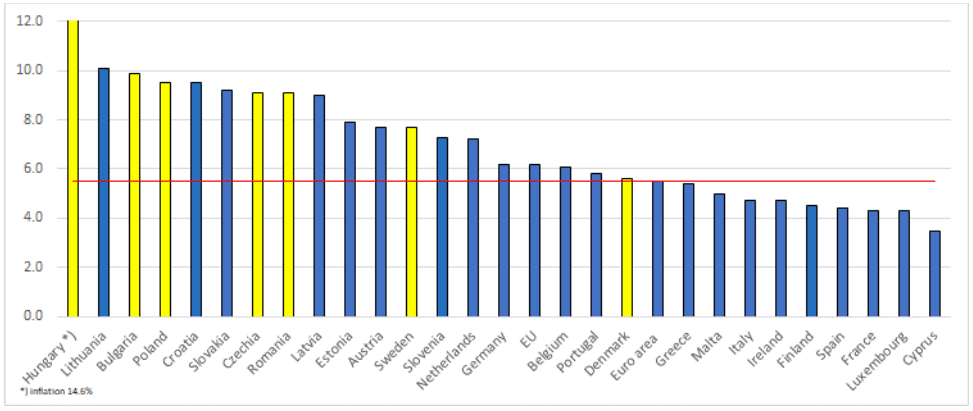

As far as core inflation is concerned, there is some good news for the ECB and some not-so-good news.

The good news is that the spread between inflation rates in the different countries is much lower than that for the HICP. The less good news is that the weighted average inflation in the eurozone is slightly higher, at 5.5% in July 2023.

Figure 2 HICP inflation ex. food and energy July 2023 source Eurostat

With or without food and energy, inflation in the eurozone is still way too high for the ECB, which led to another increase in interest rates at its recent September meeting. There is still a long way to go to reach 2%, given the tightest labour market in decades and public sectors that are all running substantial deficits.

ECB monetary policy decision for the remainder of 2023

The ECB’s Governing Council will have to weigh a lot of factors into its rate decisions for the rest of the year.

In its most recent monetary statement, the ECB noted that its inflation forecasts for 2023 and 2024 have increased. It is still difficult to see a path where interest rates will not be raised at least once more in 2023 if there are additional negative surprises on the inflation front, especially as oil prices are starting to rise again and the base effect from higher energy prices in 2022 is diminishing.

This is also along the lines of comments made by the ECB board:

“We will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, our interest rate decisions will be based on our assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission”.

Financial markets are not providing better forecasts

It is quite common for financial analysts to justify their forecasts for both interest rates and equity markets with the phrase “the forward curve shows that the market expects the central bank to lower interest rates” to this or that.

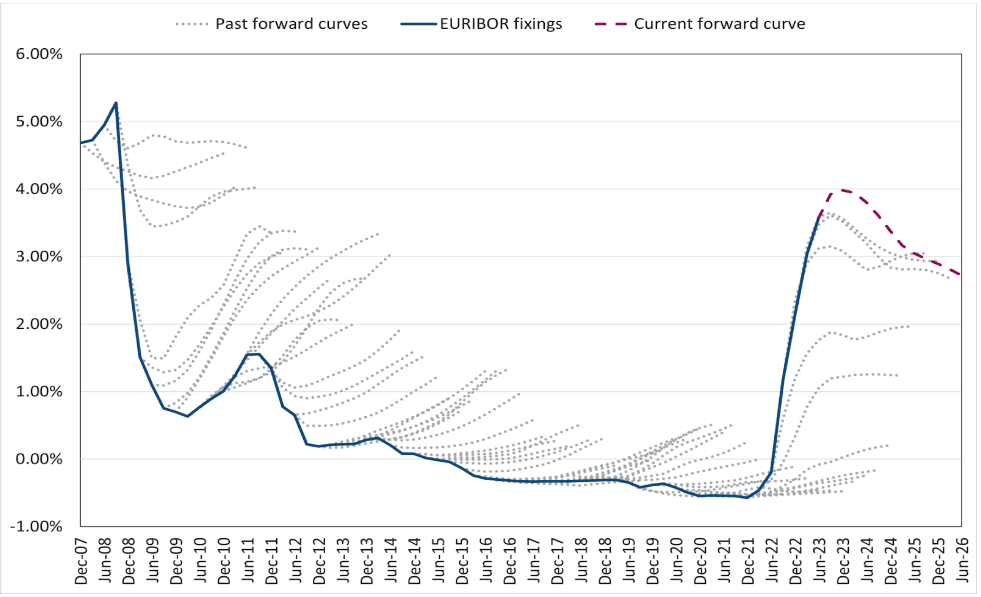

Chatham Financial has collected historical forward curves for the euro since 2007 and compared these with actual fixing rates for 3-month EURIBOR.

In other words, for each quarter since December 2007, Chatham has, based upon observed interest rates in the market, calculated the string of 3-month interest rates that would be the implied “forecast” of the financial market.

The result, to put it bluntly, is not very impressive!

Figure 3-month EURIBOR vs historical forward curve source Chatham Financial

Each “past forward curve” in the above graph shows the expectation of the financial market at that point in time.

Beyond 3-6 months, there is little to suggest that the market predicts future interest rates with any degree of accuracy.

Furthermore, 3-6 months is about the same period as the next 2-3 meetings at a central bank, where central bankers are quite outspoken about their intentions.

In Figure 3, above, there are around 66 past forward curves, and the financial market might have got it right once or twice up to 24 months. Therefore, there is absolutely no reason to trust market forecasts beyond 3-6 months.

When the next time financial analysts and commentators say that the market expects central banks to increase or decrease interest rates by X%, do not give it any credence for any period longer than two quarters.

In the past, the financial market has been wrong about the euro, the US dollar and the pound sterling, and it is unlikely that this poor track record will improve going forward.

Currently, the market forecasts a top in the 3-month EUR interest rate of 4% before the end of 2023, and that the ECB should then lower interest rates by approximately 1 %-point during 2024.

As illustrated above, the market is rarely correct in its implied forecasts, and will presumably not get it right this time either.