19/02/2024

Quantrom P2P Lending – investor return breakdown

Newsletter #67 - February 2024

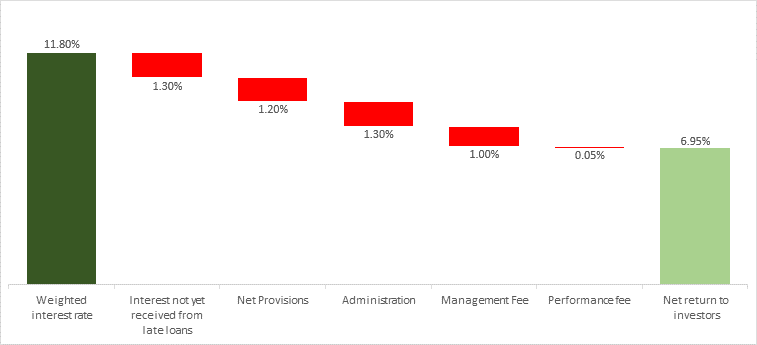

Figure 1 From gross interest on portfolio to net interest to investors

Combining stock and flows

All the information used in these calculations can be found in our monthly reports or in the Financial Statement for 2023 (FS 2023), which will be published shortly.

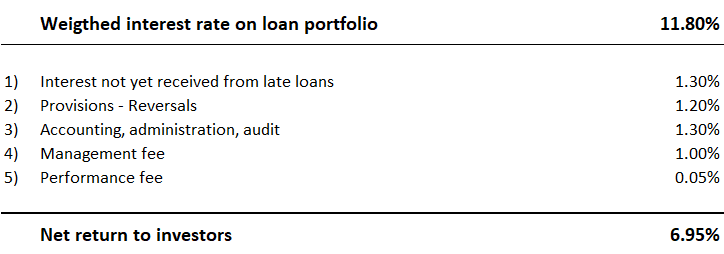

The starting point is the weighted average interest rate of the portfolio of loans. Of course, this varies all the time, but we estimate that, given the monthly weighted average interest on our portfolio, the average interest rate on the portfolio was approximately 11.80% in 2023.

Interest not yet received from late loans is detailed in the monthly reports as the percentage of late loans in the portfolio.

Provisions and reversals are also contained in the monthly report, as well as in FS 2023, and, given the estimated average size of the portfolio for 2023, converted into percentage points of interest.

Accounting, administration and audit costs, also stated in FS 2023, are likewise converted into percentage points of interest rate and deducted from the weighted average interest on the portfolio.

In table below, the different deductions from weighted interest rate on the portfolio is listed resulting in the Net return to investors.

Interest not yet received

When investing in alternative lending, one thing is certain: Not all interest payments will be on time.

During 2023, an average of 11.5% of the QP2PL portfolio was more than 60 days late (loans late less than 60 days will be ignored for this calculation). As we do not register any income until the actual interest payments hit our account, there is naturally a drag on interest received. 11.5% of weighted interest on the loan portfolio is approx. 1.3% in drag on the interest received.

It is important to understand that, while QP2PL does not receive interest and therefore does not register the interest payments, in accordance with our accounting principles, interest is still payable as agreed in the loan agreement at some point in time. However, that “some point” will be in the future when the loans are settled.

Provisions – reversals

Provisions deducted for the reversals on the real estate portfolio in 2023 were larger than previous years, and amounted to 1.2% of the value of the portfolio. That 1.2% covers new provisions of approx. 2.0% and reversals equal to 0.8% of the value of the portfolio.

QP2PL follows strict accounting policies. If a loan is more than 240 days late, we will take a provision of 50% on the principal amount outstanding. We do not take provisions for loans with a loan to value (LTV) of less than 35%.

On our property-related portfolio, we know from the monthly report that the loans in the QP2PL portfolio have an average LTV of just under 50%. After provisions, a property would have to be sold for less than 25% of its estimated value before a loss would occur, although such a scenario, while indeed possible, is extremely unlikely

If a property with a provision on a late loan is sold or refinanced, then a reversal of the previous provision will take place and any late interest payments will be recorded in the income statement.

Accounting, administration and audit

Every company has costs associated with accounting, administration and audit. In the case of QP2PL, these amount to approx. 1.3% per annum, which is at an acceptable level given the size of the company and the services provided.

Management and performance fee.

The management fee is 1% and performance was approx. 0.05% in 2023.

Additional comments

What can be expected going forward? QP2PL will most likely continue to be able to generate returns to investors of between 6.75% and 7.75% on an annual basis.

Our largest exposure is towards car loans, which have been very stable over the lifetime of Quantrom P2P Lending, and we do not expect this to change in the foreseeable future.

Personal loans have also been quite stable, except for lack of settlement of pending payments from one single loan originator. Recently, however, we did receive the agreed payments from this source and do not now expect significant problems in this regard going forward.

At this point in time, we already know that loan originators have taken advantage of the lower interest rates in bond markets and refinanced some of their alternative lending, which has, in turn, resulted in a lower weighted interest rate in our portfolio.

Elsewhere, we estimate only minor provisions on our property portfolio for the coming six months. We expect recoveries in that segment going forward, which will give a positive impact on the monthly results through reversals and interest paid.