17/04/2024

Credit spreads at pre-crisis levels

Newsletter #69 - April 2024

Impact of excess liquidity

Since the failure of Silicon Valley Bank in October 2023, the Federal Reserve has provided banks with additional lending facilities and thereby liquidity. In particular, this was intended to help regional banks with regard to unrealised losses on their bond portfolios.

Flooding the market with more liquidity has worked, and the S&P 500 has now had positive returns for five consecutive months.

Naturally, this has also had an impact on credit spreads, which have narrowed to levels last seen before the financial crisis of 2008.

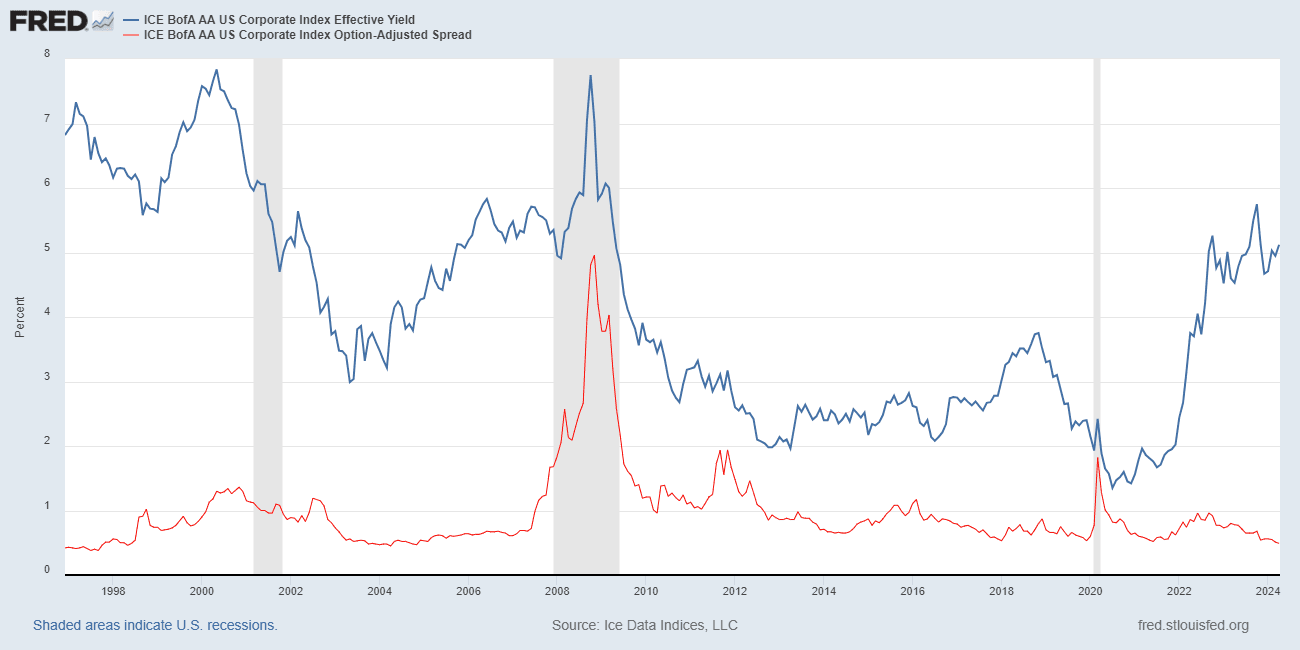

Credit spreads in investment-grade bonds

Using the ICA BofA AA US corporate bonds index as a proxy for the development in credit spreads for investment-grade bonds, the spread over US Treasuries is now back to its lowest levels.

As seen in Figure 1, below, the credit spread for AA corporate bonds is down to levels not seen since before the dot.com bubble of 2000 and the financial crisis of 2008 - a spread over Treasuries of less than 0.5%-point.

Figure 1 ICE BofA - US AA-rated corporate bonds

Yields on AA-rated corporate bonds have increased significantly since the Federal Reserve began to raise interest rates, but credit spreads have, ever since the market started to expect an economic soft landing, narrowed again to levels close to all-time lows.

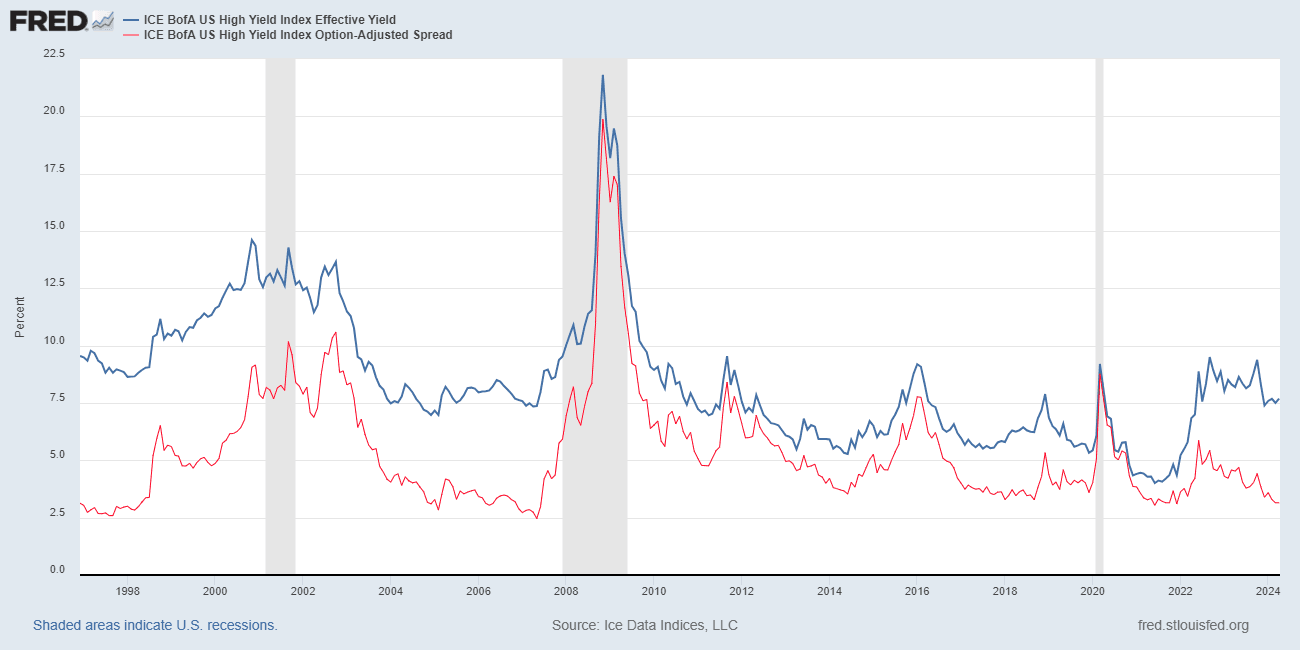

High-yield spreads

The trend in AA-rated corporate bonds is also evident in high-yield corporate bonds.

Figure 2, below, shows that credit spreads for high-yield bonds have dropped to the lows seen before the dot.com bubble and the financial crisis.

An interesting observation regarding interest on high-yield bonds is that the current level of around 7.5% is the same as it was before the financial crisis.

“Normally”, credit spreads narrow when the economy is doing well, as they did in the period 2002-2006. Now, credit spreads have narrowed because the Federal Reserve has aggressively hiked interest rates, while simultaneously providing ample liquidity to the financial system.

This “anomaly” in the behaviour of credit spreads can most likely be attributed to the excess liquidity provided.

Figure 2 ICE BofA US High yield corporate bonds

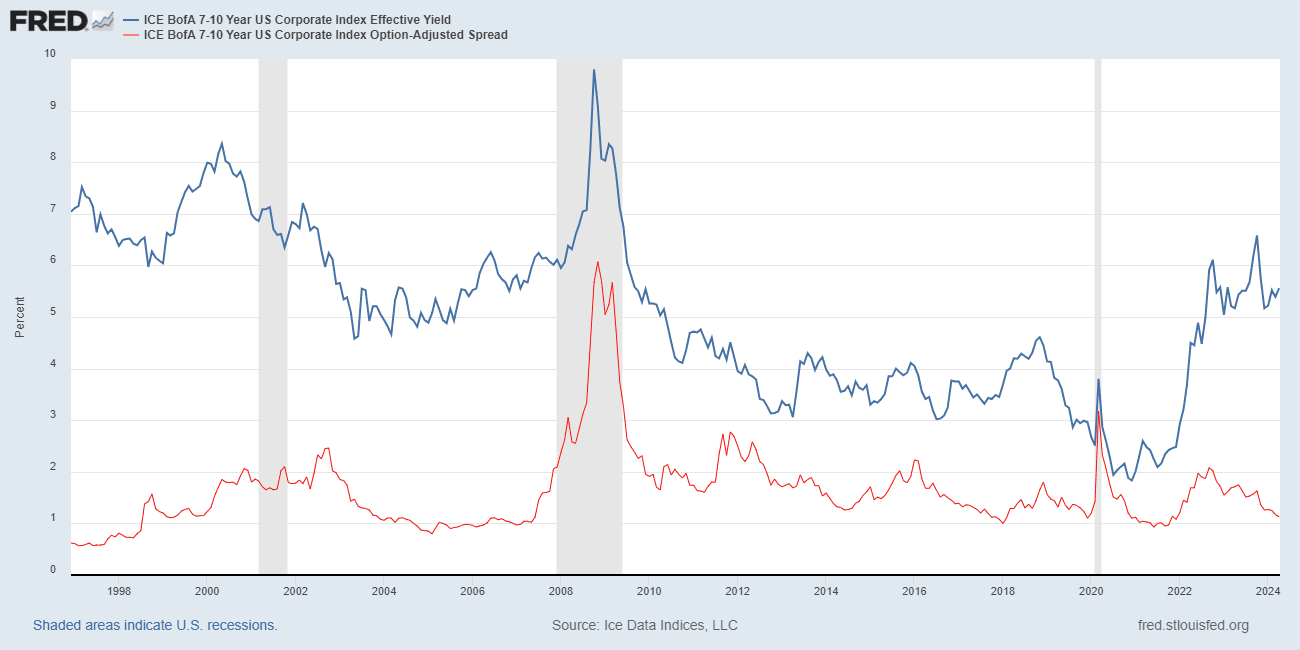

Credit term structure

The development of credit term structure since 1996, as shown in Figure 3, below, is very interesting.

Figure 3 ICE BofA 7-10 Year US corporate bonds

Although we should be in a situation where we are battling inflation and a slowdown in the economy due to an increase in overall interest-rate levels, there is hardly any premium for holding longer-dated corporate bonds.

In other words, the financial markets currently do not believe that there is a much higher risk for defaults in the corporate sector than for Treasuries over the next 7- 10 years.

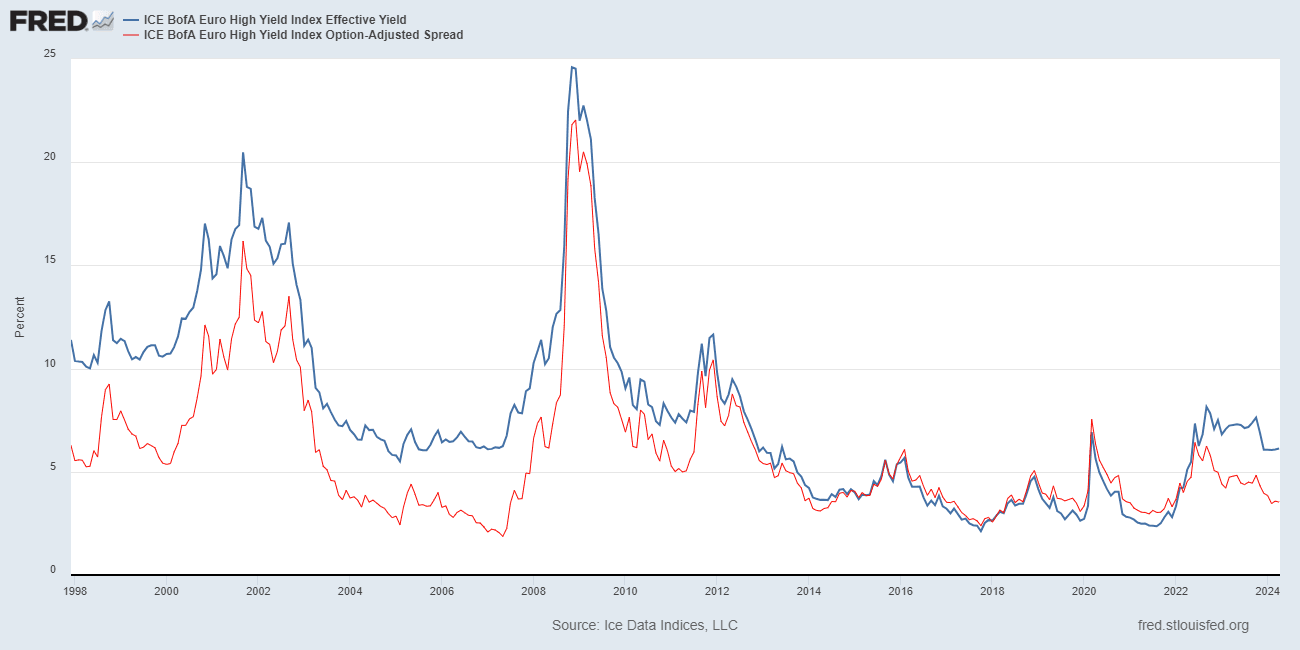

Euro high-yield credit spreads

The credit spread for euro high-yield corporate bonds is not as tight as for US high-yield corporate debt, but their yield is still very low at just over 5%.

While this reflects the overall lower interest-rate level in the eurozone, it does not change the fact that credit spreads are also extremely low given the current economic situation.

Figure 4 ICE BofA Euro High Yield corporate bonds

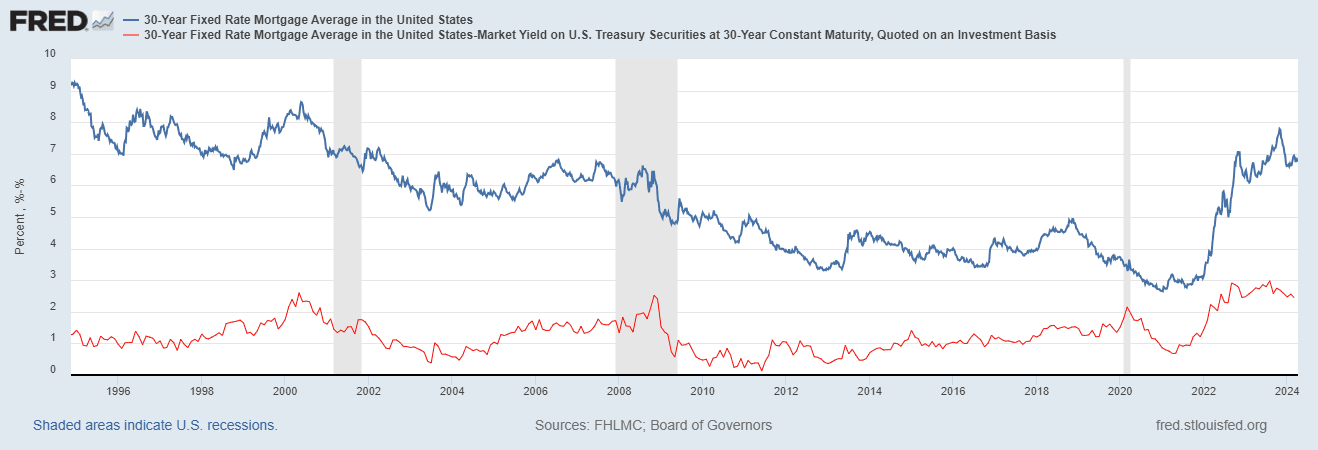

Mortgage bonds are the exception

Conventional wisdom would imply that mortgage bonds would be in a very tight credit spread to Treasuries given the credit spreads on all types of corporate bonds.

However, this is not the case, as seen in Figure 5.

Figure 5 US 30-year Mortgage bonds

The credit spread for US mortgage bonds in the 30-year segment is close to its highest levels of the last 25 years at over 2.5%-points with an overall interest of around 7%.

One must therefore wonder how we have ended up in a situation where high-yield corporate bonds are trading at or around the same interest-rate levels as secured mortgage bonds.

There is probably no definitive answer to this question, although a combination of unwise fiscal and monetary policies in both the US and Europe has clearly contributed to taking the financial system out of balance.