21/01/2025

Inflation Revisited: is EU Inflation bouncing off 2%?

Newsletter #77 - January 2025

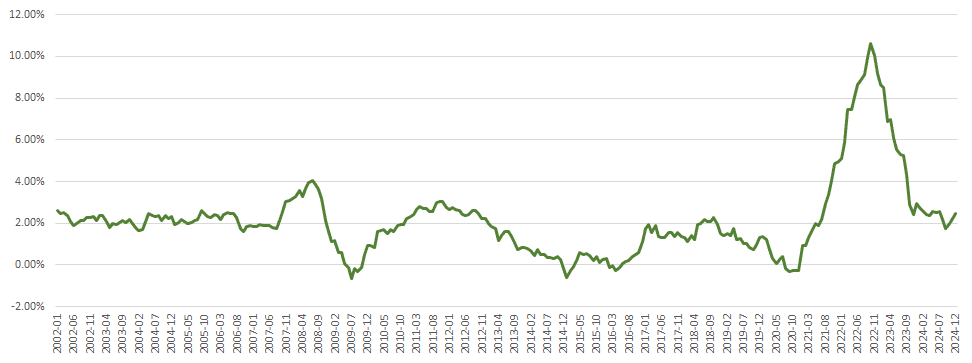

The European Union has faced a turbulent inflationary landscape since the inflation surge of late 2022, which was attributed to the aggressive fiscal and monetary measures deployed to combat the economic fallout from COVID 19. These policies, while essential for recovery, inadvertently overheated economies across the eurozone. As a result, inflation spiked dramatically, but the subsequent year saw a marked deceleration in price increases. By early 2024, however, this downward trajectory appeared to have plateaued, as illustrated in Figure 1, below.

Figure 1 HICP annual inflation - eurozone

Despite a brief dip in September 2024, when the Harmonized Index of Consumer Prices (HICP) inflation dropped below 2%, due to a significant fall in energy prices, inflation had rebounded to 2.4% by December. The critical question now is whether inflation is on an upward trajectory again. To better understand the dynamics at play, we will examine the main components of the HICP, highlighting their contributions to overall inflation trends and the implications for future monetary policy.

Examining the key components of inflation

Inflation is a multifaceted phenomenon, influenced by various sectors within the economy. To gain clarity on the trajectory of eurozone inflation, it is essential to break down the main components of the HICP: food, energy, services and non-energy industrial goods.

Food inflation

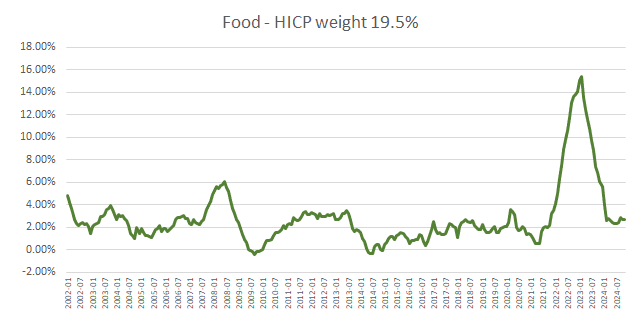

Food prices have demonstrated a relatively stable pattern following the sharp increases observed in 2022. After peaking alongside other inflation components, food inflation then began to decline steadily, bottoming out during the summer of 2024. Over the past nine months, food inflation has maintained an annual rate of between 2.5% and 2.8%, as illustrated in Figure 2, below.

Figure 2 Food inflation - eurozone

This stability, however, is not indicative of a return to pre-2022 conditions. The sustained rate of food inflation reflects structural factors, such as elevated production costs, labour market dynamics and higher energy prices. From 2014 to 2021, food inflation often hovered below 2%, but achieving such levels consistently under the current economic environment seems improbable. Unless significant changes occur in global commodity prices or agricultural productivity, food inflation is likely to remain above the 2% threshold for the foreseeable future.

Energy Inflation

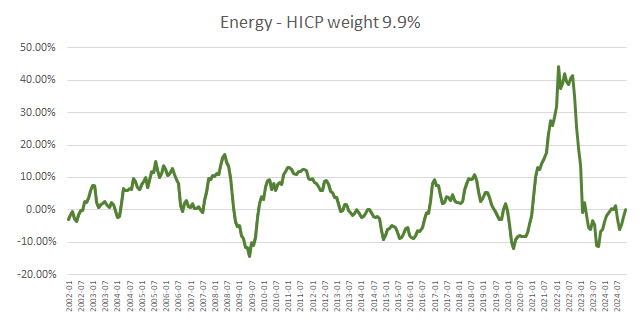

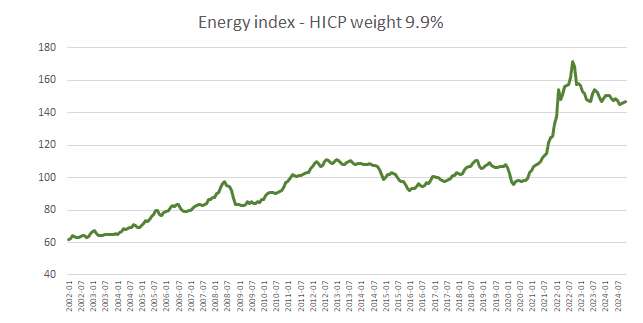

Energy inflation is notoriously volatile, with fluctuations often exceeding 10% year-on-year. This volatility was starkly evident during and after the energy crisis of 2022. Although energy prices have moderated somewhat since their peak, the effects of the 2022 spike have not been entirely reversed. Below, Figure 3, underscores the erratic nature of energy inflation, while Figure 4 demonstrates that the HICP energy index remained approximately 40% higher at the end of 2024 compared with 2020.

Figure 3 Energy inflation - eurozone

This persistent elevation in energy prices has profound implications. Higher energy costs directly impact living expenses for households and reduce the competitiveness of European businesses, which now face significantly higher production costs. While some energy price volatility may normalize in the short term, structural factors, such as geopolitical uncertainties, the transition to renewable energy and supply chain disruptions, suggest that energy inflation will remain a critical contributor to overall inflationary pressures in the eurozone.

Figure 4 HICP Energy index

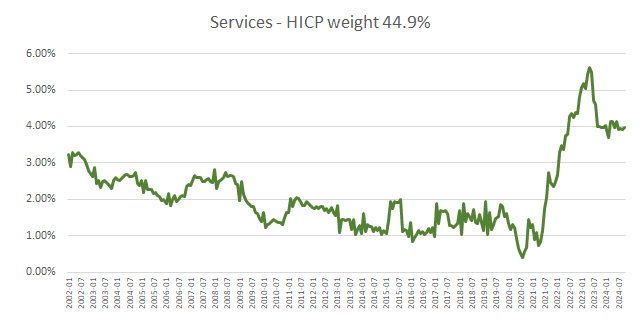

Services

Services inflation represents the largest component of the HICP and has exhibited a troubling trend. Unlike food and energy, services inflation shows little sign of retreating to pre-COVID 19 levels. Figure 5 highlights this stagnation, with inflation consistently hovering around 4%.

This persistent inflation in services can be attributed to two primary factors: robust wage growth and stagnant productivity. Labour shortages across various sectors have driven wages upwards, while gains in productivity have failed to keep pace. Given these dynamics, services inflation is unlikely to fall significantly in the near term. Policymakers may find it particularly challenging to influence this component through traditional monetary tools, as it reflects deeper structural issues in the labour market and service-sector efficiency.

Figure 5 Services inflation - eurozone

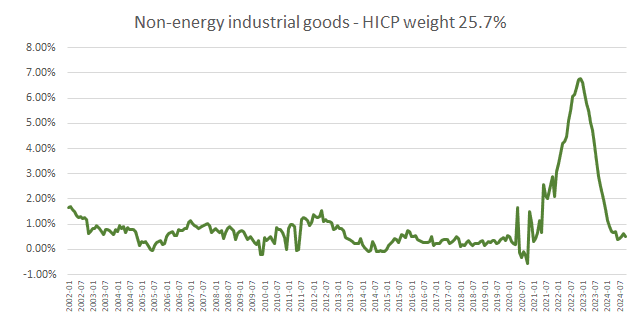

Non-energy industrial goods

Non-energy industrial goods inflation has demonstrated a more promising trend, nearly returning to pre-COVID-19 levels. As seen in Figure 6, inflation in this component has fallen below 1% in recent months, reflecting a normalization of supply chains and a stabilization of manufacturing costs.

However, this recovery is not immune to external shocks. The inauguration of the new US administration in January 2025 has raised concerns about potential tariffs and trade barriers, which could trigger a one-time spike in prices for non-energy industrial goods. Geopolitical instability and protectionist policies remain key risks to this sector's inflation outlook.

Figure 6 Non-energy industrial goods inflation - eurozone

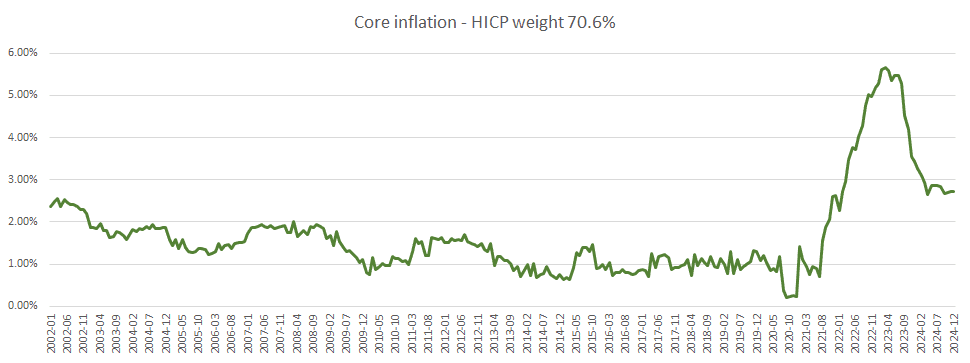

Core inflation: the ECB's measure of price stability

Core inflation, which excludes the volatile components of energy and food, is a critical metric for assessing underlying inflationary pressures. The ECB has consistently argued that core inflation is on a downward trajectory, justifying interest rate cuts from early 2024. According to the ECB's latest projections, core inflation is expected to decline from 2.9% in 2024 to 2.3% in 2025 and eventually reach 1.9% by 2026-2027.

However, these projections have raised scepticism. Core inflation is heavily influenced by services and non-energy industrial goods, both of which exhibit limited downward momentum. Figure 7, below, illustrates that core inflation has plateaued in recent months, with equal probabilities of an upward or downward shift.

The ECB's optimistic forecasts may be interpreted as an effort to align expectations with policy targets rather than reflecting the realities of economic trends. The bond market appears to share this scepticism, as evidenced by the recent increase in yields on 10-year German bonds, which has risen by 0.5 percentage points since October 2024 to approximately 2.5%. This rise indicates market expectations of higher long-term inflation.

Figure 7 Core inflation -eurozone

Implications for monetary policy and the economy

The current inflationary environment presents a complex challenge for policymakers. While headline inflation has moderated since its 2022 peak, structural factors within key HICP components, particularly services and energy, suggest persistent upward pressure.

The ECB faces a delicate balancing act. Premature rate cuts could risk reigniting inflationary pressures, while prolonged tightening might stifle economic growth. Policymakers must also contend with external factors, such as geopolitical risks and global trade dynamics, which could further complicate inflation management.

For businesses and consumers, the implications are equally significant. Elevated energy costs and persistent services inflation erode purchasing power and profitability, creating headwinds for economic recovery. Households, particularly those in lower-income brackets, face continued strain as the cost of living remains elevated.