17/02/2025

Is our macro case still valid?

Newsletter #78 - February 2025

Assessing the validity of our macro investment case

As long-term investors specializing in credit markets, it is essential to regularly evaluate the macroeconomic conditions that underpin our investment strategy. The evolving economic landscape, particularly within the European Union (EU), necessitates a thorough analysis to determine whether our investment thesis remains intact. In this memo, we revisit the rationale for investing in the Baltic states and Romania, examining key macroeconomic indicators, structural trends and potential risks.

Economic convergence with Germany: a key indicator

A primary measure of economic progress and integration within the EU is GDP per capita. This metric allows us to assess whether Eastern European member states continue to close the economic gap with Germany, the region’s largest economy.

GDP per capita trends

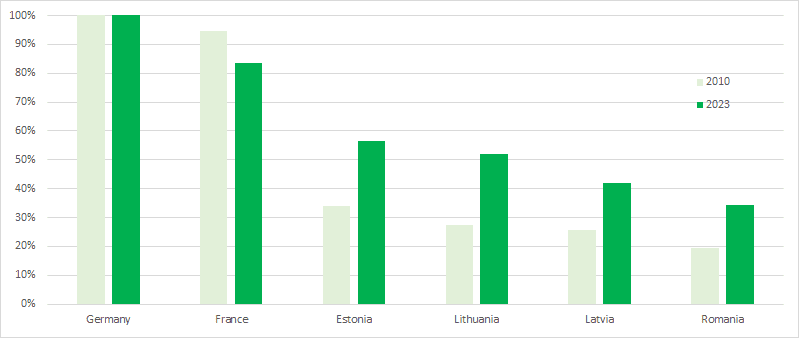

Figure 1, below, presents nominal GDP per capita for 2023, benchmarked against Germany (source: Eurostat). The data reveals clear trends in economic convergence:

- France: declined from 95% of German GDP per capita in 2010 to 83% in 2023, reflecting economic stagnation;

- Estonia: increased from 34% in 2010 to 56% in 2023, showing strong economic momentum;

- Lithuania: rose from 27% to 52%, demonstrating substantial growth;

- Latvia: improved from 26% to 42%, indicating steady progress;

- Romania: advanced from 19% to 34%, maintaining upward momentum, despite lagging behind the Baltic region.

Figure 1 - 2023 Nominal GDP per capita in EUR compared with Germany (source Eurostat)

These trends confirm that Eastern EU economies are continuing their convergence process, reinforcing their attractiveness for long-term investment. The implications for investors are significant, as these markets offer strong growth potential with relatively lower risk than in previous decades.

Real GDP growth and productivity: challenges in Western Europe vs. opportunities in the East

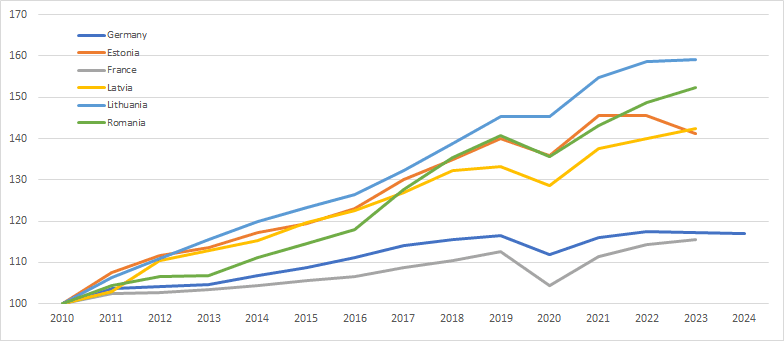

In addition to GDP per capita, real GDP growth provides insight into the economic trajectory of different EU member states. Figure 2, below, illustrates the GDP volume indices from 2010 to 2023 (source: Eurostat), highlighting disparities in economic performance across Europe.

Key Observations

- France and Germany: have grown by less than 20% in real terms over the period, indicating sluggish economic expansion;

- Slow productivity growth: structural inefficiencies and failure to implement comprehensive structural reforms have hampered economic performance;

- Eastern Europe’s rapid growth: Lithuania, for example, has nearly triple real GDP growth compared with France and Germany, illustrating its positive economic development.

Figure 2 GDP – chain-linked volumes index 2010 = 100 (source Eurostat)

These trends highlight the broader challenges facing Western Europe, including mounting political dissatisfaction and increasing pressure on governments to implement economic reforms. In contrast, Eastern Europe’s strong performance suggests continued opportunities for investment.

Fiscal stability and public debt: a comparative analysis

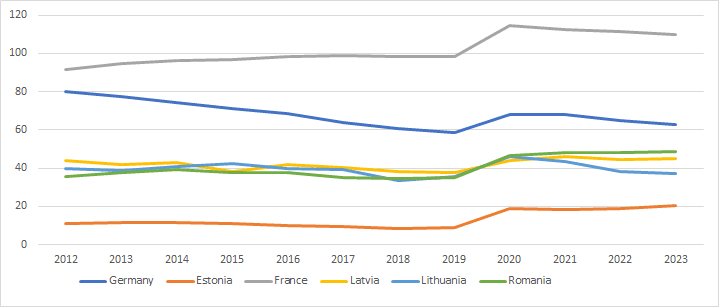

Fiscal health remains a key factor for investors assessing sovereign and corporate credit markets. Figure 3 (source: Eurostat), below, presents the general government debt levels as a percentage of GDP, offering insights into fiscal discipline and economic resilience across EU member states.

Debt and fiscal policy trends

- Baltic States and Romania: maintain significantly lower public debt levels compared with Germany and France, offering greater fiscal stability;

- Defence spending commitment: the Baltic states allocate approximately 3% of GDP to defence spending, meeting NATO’s recommended target;

- France’s fiscal challenges: persistent budget deficits continue to pose risks, particularly if defence expenditures need to increase.

Figure 3 General Government Debt as a percentage of GDP (source Eurostat)

Lower debt burdens in Eastern Europe suggest these economies have greater flexibility for fiscal stimulus and economic resilience in the event of future economic shocks. This provides an additional layer of security for investors considering exposure to these markets.

Investment risks and considerations

While the macroeconomic case remains strong, investors should be aware of potential risks, including:

- geopolitical uncertainty - proximity to Russia and potential regional tensions could introduce volatility in Baltic investments;

- inflationary pressures - rising inflation across Europe could impact purchasing power and economic stability;

- global economic slowdown - a broader economic downturn could affect exports and GDP growth, even in high-growth markets.

Conclusion: a strong and sustainable investment case

Based on a comprehensive review of macroeconomic data and fiscal stability, we reaffirm that the investment case for Eastern European EU members remains robust. These economies continue to experience rapid growth, maintain low debt levels and implement favourable economic policies, making them highly attractive for long-term investors.

Despite historical risk premiums associated with investing in the Baltic states and Romania, such concerns are increasingly disconnected from macroeconomic fundamentals. This presents a compelling investment opportunity for those seeking growth-oriented exposure within the European Union.

As always, we remain vigilant in monitoring economic developments and will continue to refine our investment strategy to align with the evolving market landscape.