19/05/2025

On Deals and Debt

Newsletter #81 - May 2025

Federal Reserve did not move

In their latest May meeting, the Federal Reserve opted not to adjust interest rates, emphasizing ongoing uncertainty in the economic outlook. This cautious stance effectively signals skepticism toward the Trump administration's optimistic economic forecasts and their ambitious growth strategies. The Federal Reserve’s position suggests the central bank harbors concerns about the potential volatility stemming from current economic policies and international trade dynamics.

Trade deals and tariffs

Turning specifically to recent trade developments, the much-publicized US-UK trade agreement—touted as the first of many bilateral deals aimed at reshaping America's global trading relationships—highlights the complexities and contradictions inherent in such negotiations. Despite official claims of significant tariff reductions, the reality of the agreement presents a mixed picture. For instance, car imports from the UK to the US will now face a practical tariff rate of 10%. This tariff replaces a previously inflated, largely symbolic 25% tariff but applies only to the first 100,000 vehicles. Additional "reduced rates" are selectively applied to certain goods, limiting broader economic benefits.

Additionally, favorable provisions have been included for American tech giants, effectively shielding them from IT-related taxes within the UK. This illustrates a deal clearly designed to provide targeted benefits rather than fostering broad-based economic cooperation.

Another notable component involves aviation giant IAG, parent company of British Airways, Aer Lingus, and Iberia. The company agreed to purchase Boeing 787 aircraft valued at approximately USD 10 billion, though this arrangement specifically applies only to British Airways. Concurrently, orders were placed with Boeing's European rival, Airbus, for 21 A330-900neo planes intended for Aer Lingus and Iberia. This strategic diversification anticipates the European Union’s proposal to introduction of tariffs on Boeing aircraft, signaling significant risk aversion to potential trade disputes.

Such carefully tailored agreements underscore a broader caution: trade deals orchestrated under the Trump administration tend to prioritize narrow, politically advantageous interests rather than comprehensive economic integration. These deals appear structured primarily to reward Trump’s political allies and key industries that support his administration, rather than promoting genuine market liberalization.

Indeed, modern trade relationships rely heavily on complex regulatory frameworks, standards alignment, and reciprocal acceptance of business practices rather than mere tariff adjustments. Tariffs themselves have become increasingly marginal tools in international trade policy. As evidenced by the administration’s recent decision to temporarily reduce tariffs on Chinese imports for a period of 90 days, tariff policies under Trump remain unpredictable and potentially destabilizing.

This approach to trade raises critical fiscal concerns. With tariffs fluctuating unpredictably, revenue projections become increasingly uncertain. The resultant shortfall in tariff revenues—combined with substantial tax relief proposals and looming economic slowdown—threatens to exacerbate already significant federal budget deficits. Trump's short-term "deal-making" approach thus risks creating significant fiscal imbalances that could compound the negative economic consequences of a future downturn.

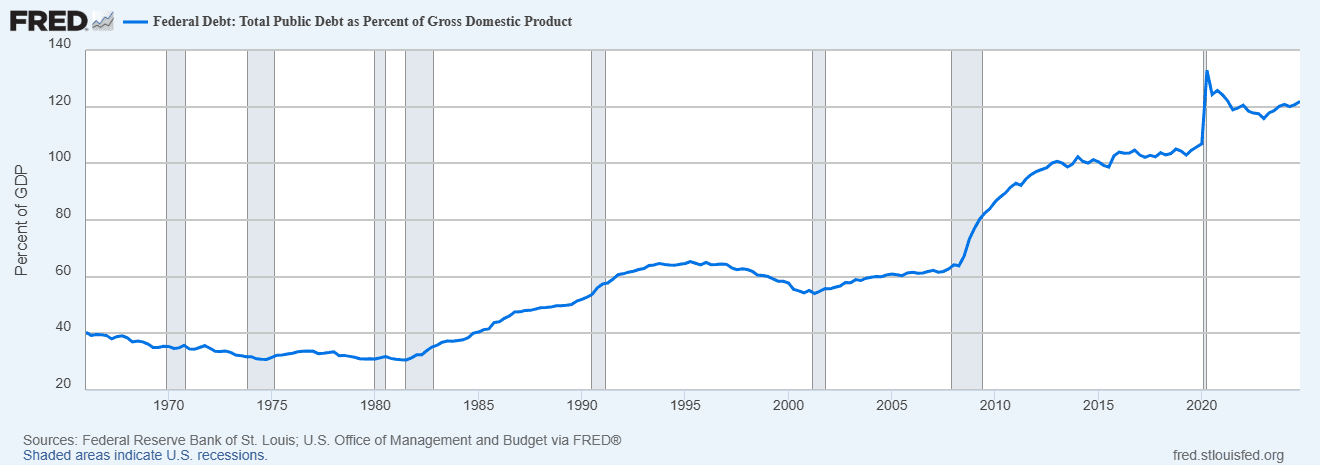

US debt is accumulating.

The accumulation of U.S. federal debt has reached notably high levels compared to most EU countries, as illustrated in Figure 1. U.S. federal debt peaked significantly during the 2020 pandemic crisis and has not substantially declined since. The modest reductions observed have primarily been driven by nominal GDP growth and inflation rather than explicit fiscal consolidation efforts.

Figure 1 US Federal debt as % of GDP

Running annual budget deficits of approximately 5-7% of GDP is unsustainable in the long run. Historically, the global dominance encapsulated by "Pax Americana" has facilitated financing for U.S. debt. However, continuous high deficits, particularly outside wartime or significant crisis contexts, are unlikely to remain tolerated indefinitely by bond markets. Recent fiscal policies, such as those under former President Trump, including reduced tariffs and tax cuts designed as payoffs to political constituencies, risk further exacerbating budgetary imbalances. Extensions or additional tax reductions could potentially lead to severe budgetary deterioration, triggering adverse responses from financial markets.

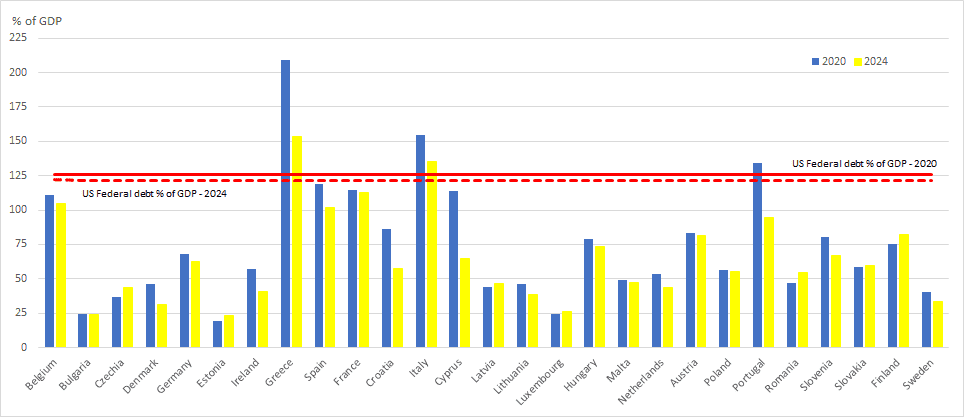

Comparison with EU Debt Levels

In contrast, many European Union countries generally exhibit lower general government debt levels compared to the U.S., as demonstrated in Figure 2. Since the pandemic, several EU member states have successfully managed to reduce their debt-to-GDP ratios more effectively than the United States.

Figure 2 EU Countries General Government debt to GDP-ratio

Among larger EU economies, Germany notably maintains a low public debt level at approximately 62% of GDP. This fiscal position provides Germany considerable room to expand public investments significantly, including critical infrastructure upgrades and enhanced defense capabilities.

Meanwhile, countries such as Estonia, Latvia, and Poland, despite maintaining stable debt-to-GDP ratios due to substantial defense expenditure, demonstrate clear strategic benefits. Poland, notably, has developed one of the most extensive and technologically sophisticated military forces within the EU. This underscores how focused fiscal investment, even without significant debt reduction, can yield significant strategic and military advantages.

Collectively, the European Union has considerable scope to strategically allocate resources towards defense, infrastructure, and research and development, aligning with recommendations outlined in the influential Draghi Report. Such investments could significantly enhance the region’s economic and geopolitical strength in the coming years.

Defence in a European Context

As previously established, the European Union (EU) and its member states have the fiscal capacity necessary to substantially increase defence expenditure. A recent joint study by the Bruegel think tank and the Kiel Institute for the World Economy assessed the requirements for European rearmament in the hypothetical absence of U.S. military support.

The study estimates that the EU and the United Kingdom would need to increase defence personnel by approximately 300,000 troops and raise annual defence spending by around EUR 250 billion. The authors point out that such a military expansion has historical precedent, exemplified by West Germany's modernization under Chancellor Helmut Schmidt in the late 1970s.

Bruegel’s analysis significantly references Ethan Ilzetzki’s comprehensive report, "Guns and Growth: The Economic Consequences of Defence Buildups," published by the Kiel Institute.

Economic Implications of Increased Defence Spending in Europe

Ilzetzki's report underlines that increased defence spending generally stimulates economic growth through heightened output, procurement, and employment. While there remains debate on the exact magnitude and the potential crowding-out effect on private investments, the consensus suggests an overall expansionary impact.

Conservative estimates indicate that boosting defence spending from 2% to 3.5% of GDP could increase Europe-wide GDP by approximately 0.9% to 1.5%. This suggests a manageable trade-off between defence expenditure and private consumption, especially if the spending is financed by public borrowing rather than taxation. Debt-financed expenditure, particularly when temporary or front-loaded, would likely produce a positive GDP effect. In contrast, tax-financed defence expansion could diminish or even reverse the positive impact due to reduced private consumption.

The broader macroeconomic environment is crucial. The positive economic outcomes of increased defence spending significantly depend on the monetary policy adopted by the European Central Bank (ECB). A neutral or accommodative ECB monetary stance would enhance economic benefits, whereas tightening monetary policy in response to modest inflation could undermine both short-term economic stimulus and long-term productivity gains.

Procurement and Research & Development (R&D)

Currently, nearly 80% of European defence procurement originates from non-EU suppliers, which significantly restricts economic and technological gains. Shifting procurement toward European firms, particularly those developing dual-use technologies, could maximize innovation spillovers and economic returns. Additionally, prioritising smaller, innovative contractors would foster a competitive and dynamic defence industry. Introducing dual-sourcing strategies—contracting multiple suppliers across EU member states—would further enhance efficiency, promote knowledge transfer, and ensure equitable economic distribution.

Moreover, defence-related R&D investments offer substantial economic returns and extensive civilian sector spillovers. As highlighted in the Draghi Report, investing in R&D is strategically vital for bolstering Europe's structural productivity. A more integrated European approach, including coordinated defence planning, joint financing mechanisms, and consolidated procurement strategies, would enable Europe to efficiently scale capabilities and secure technological autonomy in strategic sectors.

Role of the ECB

The ECB's role is critical in sustaining economic momentum generated by increased defence expenditure. Moderate inflation due to higher public investment is not inherently destabilizing; rather, it can help reduce public debt burdens by increasing nominal GDP. Premature monetary tightening would neutralize fiscal stimulus and undermine the potential productivity advantages from defence-led investment.

Conclusion

Given the ongoing uncertainty surrounding U.S. politics under the Trump administration, Europe stands at a historic juncture.

The EU and the UK now have a unique opportunity to establish an independent, sovereign path in defence and security. Realizing this goal demands unprecedented coordination, institutional reforms, and political resolve. Success would significantly enhance Europe's strategic autonomy, economic resilience, and technological advancement, reshaping its global role for decades to come.