23/06/2025

Treasuries - Wait for it ………

Newsletter #82 - June 2025

Federal Reserve did not move again

Policy rates were held steady at the June meeting of the Federal Open Market Committee, perpetuating a cautious stance despite external outcry and media commentary.

The FOMC communiqué reiterated that while up to a 0.5 percentage‐point reduction could materialize later in 2025, the Committee remains reluctant to ease until inflation trajectories demonstrably converge toward target and labour markets exhibit sustained softness. This measured posture, unchanged from prior meetings, prompted immediate reactions - particularly on social media - underscoring the tension between market expectations for accommodation and the Fed’s insistence on data dependency.

As a result, US Treasury yields exhibited minimal net movement post‐announcement, and the yield curve’s configuration remained broadly similar to pre‐meeting levels. Market pricing continues to embed limited probability of near‐term cuts, reflecting an understanding that monetary policy will likely remain restrictive until inflation recedes convincingly and unemployment shows early signs of deterioration.

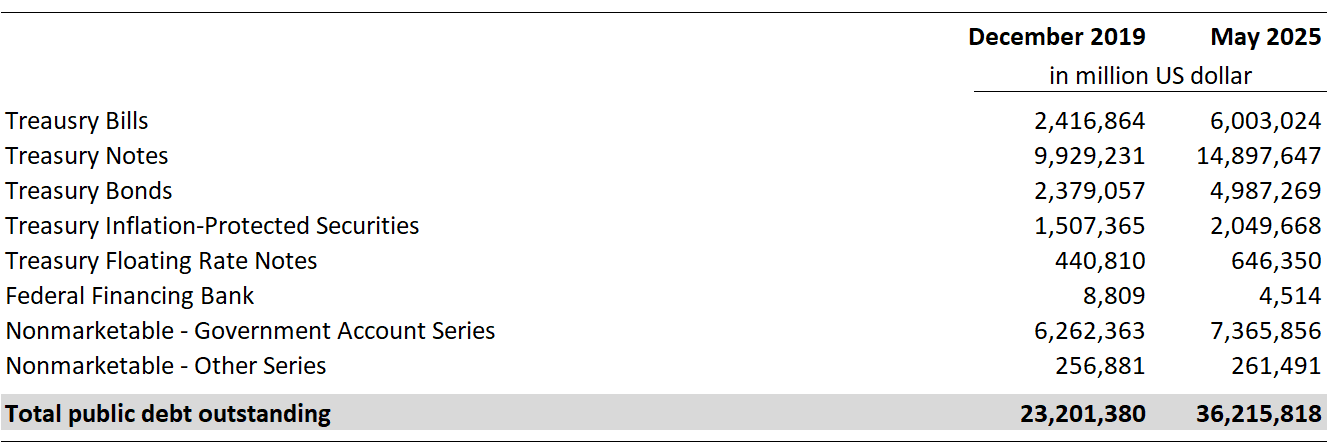

Structure of the US public debt

On a monthly basis, the US Treasury publishes comprehensive breakdowns of outstanding public debt.

Broadly speaking, obligations are divided into two principal categories:

- marketable debt - instruments auctioned in capital markets, including Treasury bills, notes, bonds, and TIPS; and

- non‐marketable debt - predominantly Government Account Series holdings, i.e. intragovernmental obligations such as the Civil Service Retirement and Disability Fund, the Department of Defense Retirement Fund, and the Federal Old‐Age and Survivors Insurance Trust Fund.

Through issuance of special‐issue securities to these trust funds, the Treasury effectively finances part of the debt internally, analogous to non-government pension‐fund purchases of US Treasuries but executed via earmarked instruments.

Table 1 US Public debt source US Treasury

Notably, between the onset of COVID‐19 and late 2024, nominal public debt expanded from roughly USD 23 trillion to over USD 36 trillion (an increase exceeding 50%), propelling the debt‐to‐GDP ratio past 120%.

This surge reflects pandemic relief measures, expansive fiscal support and persistent budget deficits that have engendered significant fiscal pressures.

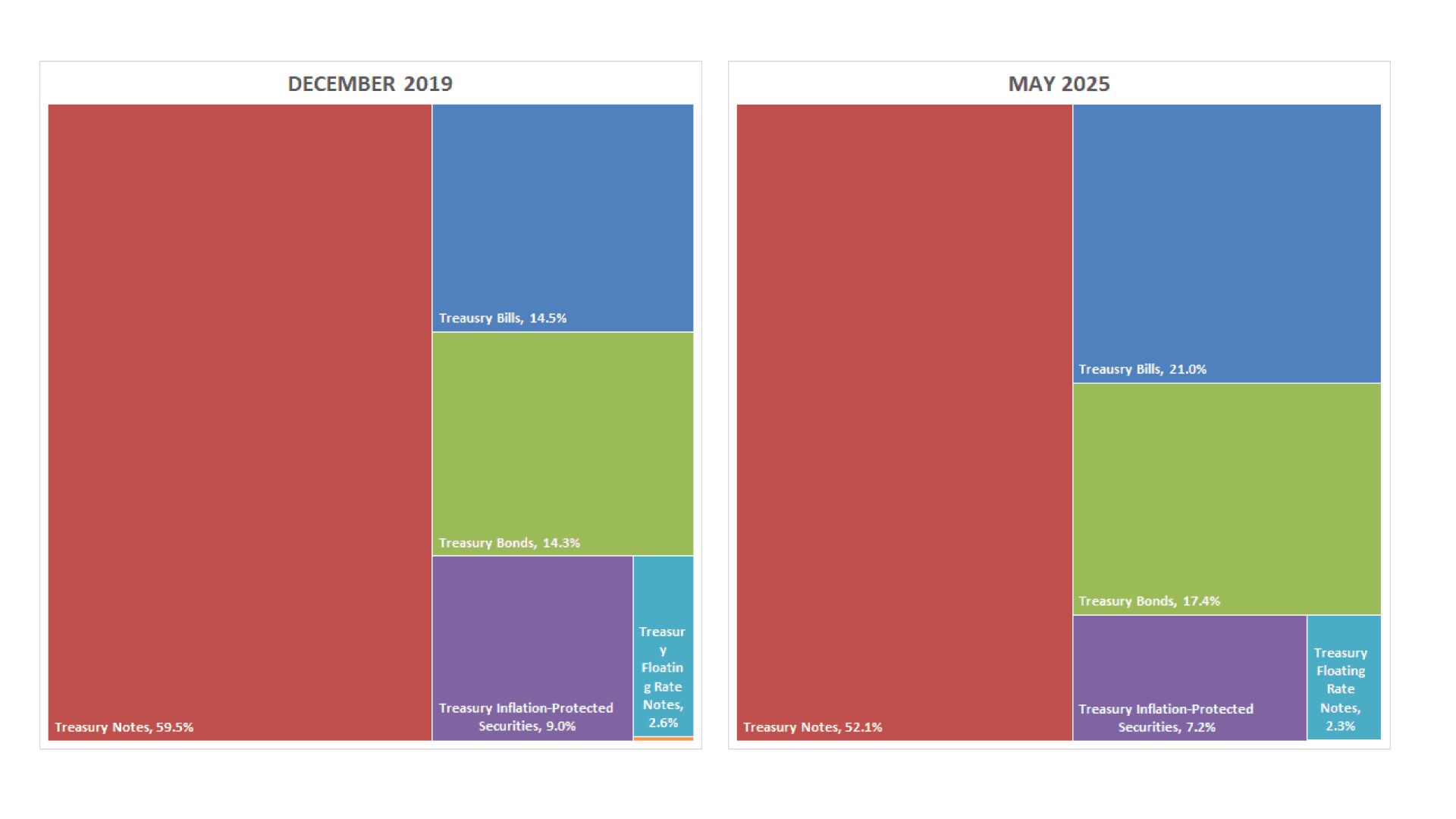

From a capital‐markets perspective, shifts in issuance patterns since end‐2019 warrant closer scrutiny.

During and after the pandemic, the Treasury ramped up short‐dated issuance - particularly Treasury bills with maturities generally up to 18 months - to meet acute funding needs. Consequently, bills now comprise approximately 21% of outstanding marketable debt, implying that over one fifth of the debt stock needs to be rolled over annually.

Concurrently, the share of intermediate‐maturity notes (2–10 years) contracted by more than seven percentage points, reflecting a strategic tilt toward shorter financing in a low‐yield environment. Longer‐dated bonds (20–30 years) saw their proportion increase by roughly three percentage points, as the Treasury sought to lock in historically low long‐term yields whenever this segment traded below intermediate‐term rates.

Figure 1 Relative size of US marketable securities source US Treasury

This reallocation, logical within an inverted or flat yield-curve framework, presents challenges with yields now normalizing, as heavy short‐term concentrations expose refinancing to elevated costs if interest rates remain higher for longer.

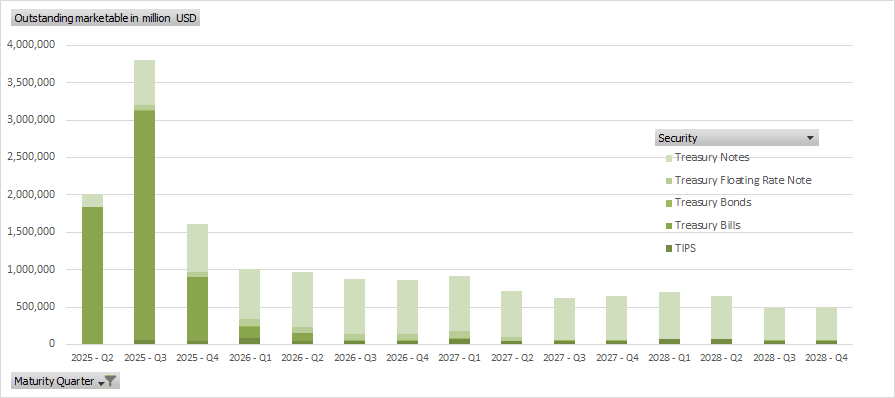

Past Treasury policy is back with a vengeance

Absent a shift toward easier monetary policy, refinancing pressure will intensify along the short end. With over 21% of marketable debt in bills, the more “cost‐effective” refinancing window (typically around 2–3 years) becomes expensive when the bulk of maturities cluster at the shortest end of the curve.

As Figure 2 (below) indicates, a substantial fraction of more than 10% of the outstanding debt will mature in Q3 2025 alone, requiring rollover at prevailing high yields.

The legacy of prior issuance in a low‐rate environment thus “returns with a vengeance”: large volumes of debt issued under very low yields now face refinancing at appreciably higher rates, amplifying interest‐expense trajectories and narrowing fiscal headroom.

Figure 2 Maturity per quarter of outstanding marketable debt source US Treasury

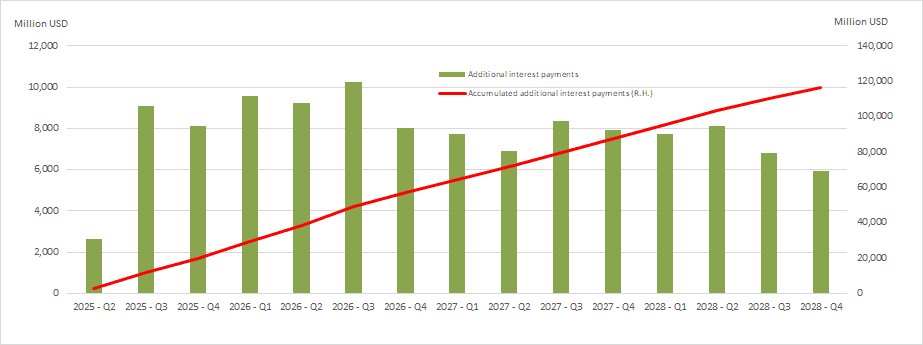

Effect of higher interest rates on Treasury notes

Based on the current outstanding portfolio of Treasury notes, we have estimated the incremental impact on interest payments through to the end of the Trump administration’s term in late 2028.

Using yields observed immediately after the 18 June FOMC meeting, we have also assumed the following:

- maturing notes will be reissued in identical maturities;

- refinancings will occur at prevailing yields for each respective maturity;

- the maturity profile will remain unchanged beyond rollovers.

Under these premises, over 9 trillion US dollars of notes will require refinancing by end-2028. Many of these were issued in the period between 2015 and post-COVID-19 when yields were at historic lows, so rolling them over at higher prevailing rates entails substantial budgetary costs.

The results of these calculations are shown in Figure 3, below.

Figure 3 Effect of refinancing Treasury Notes on interest payments source Quantrom

Our calculations show that, in terms of:

Quarterly and accumulated increases

Excluding Q2 2025, the average quarterly uptick in interest outlays from refinancing Treasury Notes is about USD 8 billion. Accumulated, this implies roughly USD 110 billion of additional interest expense per year by end 2028.

Fiscal significance

The USD 110 billion increment equals around 0.4% of current GDP, exerting noticeable pressure on the budget when primary deficits are hovering near 6% of GDP. Such sustained borrowing needs will drive further issuance, which in turn will raises future interest burdens in a self-reinforcing cycle.

Market feedback loop

As interest costs climb, investors may demand higher yields to absorb increased supply, further amplifying borrowing expenses. This dynamic limits fiscal leeway for other priorities and can heighten debt-service risk perceptions .

Comparison with defence spending

For context, the US Department of Defense budget is roughly USD 840 billion annually. If baseline interest outlays - including the incremental USD 110 billion - continue rising, total interest payments could approach or even match defence spending within a few years.

Implications for policy

When interest obligations rival a major expenditure category such as defence, trade-offs intensify, and choices about deficit reduction, spending priorities and growth-oriented measures become more acute. The Treasury’s issuance strategy (maturity mix, auction cadence) and credible fiscal plans are crucial in maintaining investor confidence and preventing yields from escalating further.

These dynamics underscore how low-rate issuance can later magnify refinancing costs to the extent that interest outlays compete directly with defence budgets, heightening pressures on the Treasury’s budgetary calculations.

Who will buy US Treasuries going forward?

International investors

International demand for US Treasuries remains pivotal to financing the US fiscal deficit, but several headwinds could temper future inflows, as listed below.

Size and composition of current holdings

As of April 2025, foreign holdings of US Treasury securities remain near record highs, at around USD 9 trillion overall, despite periodic bouts of volatility arising from tariff announcements and geopolitical tensions. Major holders include Japan (approximately USD 1.1 trillion in April 2025), the United Kingdom (around USD 800 billion) and China (USD 750 billion).

These figures underscore the persistent reliance on Treasuries as safe-haven assets and reserve instruments.

Geopolitical and trade policy uncertainty

Fluctuating trade policies and tariff rhetoric can induce episodic sell-offs or slower accumulation of Treasuries. For instance, announcements of steep tariffs have triggered temporary increases in long-term yields, prompting some foreign private investors to reduce holdings, even if central banks or official institutions have partially offset net outflows until now.

Moreover, ongoing tensions, such as those between the US and China, raise questions about currency and political risk, potentially motivating large holders to diversify into alternatives or reduce marginal purchases.

Relative yield and currency considerations

When domestic bond yields in major economies approach or exceed comparable US yields, currency-hedged returns may favour local issuance. For example, Japanese 30-year government bond yields near 3% could narrow the incentive to hold long-dated US Treasuries given the currency risk and hedging costs.

Similarly, European investors facing higher defence expenditures in Europe and fiscal pressures may seek regional sovereign bonds, particularly if the euro strengthens or offers comparable real yields.

Central bank behaviour

Some foreign central banks have begun modestly trimming exposure to US assets, reflecting portfolio rebalancing toward a wider set of reserve currencies and assets.

Nevertheless, US Treasuries’ liquidity and perceived safety still rank highly, especially during periods of global tension. The net impact will depend on how quickly alternative government bond markets deepen and whether geopolitical shifts prompt strategic reserve diversification.

Prospects and risks

Continued large-scale issuance in the US, coupled with fiscal deficits, implies substantial supply ahead. If global demand softens materially (due to shifts in reserve-management policies, improved yields elsewhere or elevated US political/fiscal uncertainty), the Treasury market may require higher yields, thus steepening the yield curve. Such repricing could have broad ramifications, including higher borrowing costs across sectors and tighter global financial conditions.

US investors

Bank portfolios and regulatory constraints

As previously discussed in these Newsletters, US banks continue to carry sizable unrealized losses on fixed-income holdings following the recent rate upcycle. While Treasuries remain high-quality liquid assets for liquidity coverage ratio purposes, further meaningful purchases may be muted as banks prioritize capital restoration and duration management in anticipation of potential rate volatility.

Pension funds and insurance companies

Pension funds and insurers maintain strategic allocations to Treasuries for liability matching, but substantial increases would likely necessitate recalibrating actuarial assumptions or shifting risk-return targets if alternative sectors offer more attractive yields. Any incremental uptake depends on funding status, regulatory capital implications and the comparative appeal of other fixed-income instruments.

Money market funds and retail investors

Money market funds and retail investors provide a flexible but limited backstop for Treasury issuance: money market funds absorb bills when short-term yields are attractive, though regulatory changes or shifts in cash-management practices can curb their capacity; retail demand via bond funds or ETFs may rise when yields outpace alternatives but remains modest relative to overall supply.

Behavioural factors, such as concerns about locking in duration or expectations of rate moves, may further temper uptake. As a result, these channels cannot absorb large-scale issuance alone, so the Treasury must balance maturity mix and yield incentives, and communicate clearly on auction schedules and liquidity conditions to attract sufficient demand.

Wait for it ……

The US dollar’s status as the premier reserve currency continues to grant substantial financing benefits, yet a tilt toward inward-looking policies and persistent fiscal deficits, without compensatory revenue measures, risks eroding Treasuries’ safe-haven appeal over time.

Were demand to falter meaningfully, the yield curve might steepen abruptly, propagating strains throughout global financial markets. In that scenario, policymakers would confront a dilemma: either lean into easier monetary conditions, heightening the prospect of renewed inflationary pressures, or embark on politically sensitive fiscal consolidation.

The “wait for it” theme thus embodies the latent tension, as large refinancing obligations loom ahead, and misjudging the timing of market repricing could trigger significant economic and financial fallout.

The US Treasury market remains the cornerstone of the financial system, but is currently behaving like a slow-moving locomotive on a predetermined track. However, without meaningful adjustments to US fiscal policy, some unforeseen events could erode confidence in the Treasury market and transform this into a runaway train.

Our best advice is to be prepared and geared up for whatever volatility lies ahead.

Summer break

We wish all readers of our Newsletter and their families a restful and rejuvenating summer break, and we look forward to returning in August.

In the meantime, stay safe and make the most of the sunshine!