20/01/2026

Euro area status

Newsletter #88 - January 2026

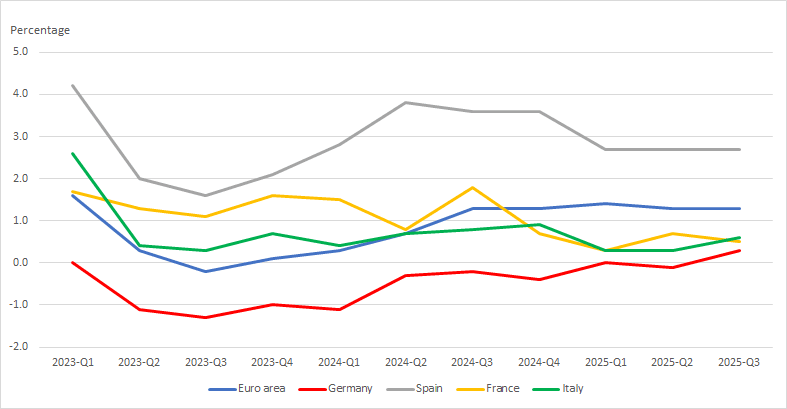

Growth

Since the COVID-19 shock, economic growth across the euro area has been largely stable, but persistently unimpressive, at about 1% per annum. Beneath this headline number, however, the country-level dispersion is material, as illustrated by the four largest economies: Germany, France, Italy and Spain.

Figure 1 GDP: year-on-year growth (source: Eurostat)

Spain, together with several smaller euro-area economies, has been expanding at close to 3%. By contrast, the three traditional engines of the euro area have been struggling to gain traction, with growth below 1% for more than three years; in Germany’s case, output has even contracted, implying recessionary conditions.

In Germany, a pivot towards higher defence and infrastructure spending should provide some incremental support to demand. In France, by comparison, the political stalemate - where even a 2026 budget agreement remains contentious - is likely to depress confidence and delay investment decisions.

At present, it is difficult in France to build a majority for structural reforms; the only durable political consensus appears to be a continuation of the current fiscal expansion, with the general government deficit running above 5% of GDP.

With municipal elections scheduled for March, political parties are positioning themselves tactically, and it is hard to envisage meaningful progress before the end of President Macron’s term in April 2027. Under the current constitutional framework, he cannot run for a third term. As a result, France is likely to remain politically and economically stalled until after the presidential election.

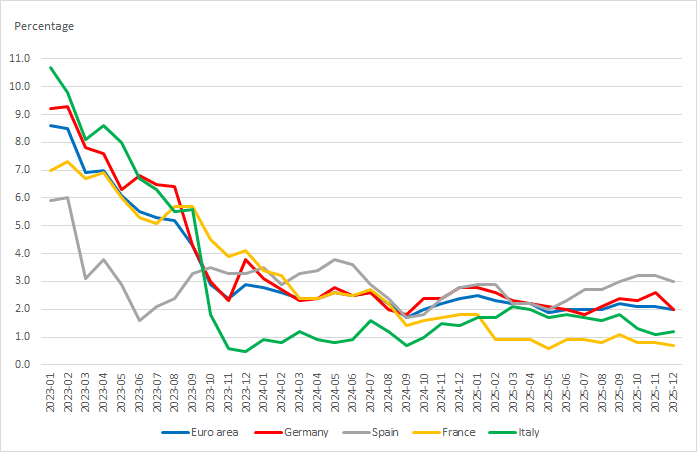

Inflation

The weak growth backdrop is also visible in the inflation data.

Overall, euro-area inflation is now close to 2%, which is broadly where the ECB would like it to be on a sustained basis.

Higher growth tends to coincide with inflation nearer the upper end of the recent range, as seen in Spain. France and Italy combine subdued activity with relatively low inflation.

Germany is a mild outlier: despite low growth, inflation remains around the 2% mark.

Figure 2 HICP: year-on-year inflation (source: Eurostat)

The ECB is likely to remain on hold

Given the current macroeconomic situation and the latest indicators, it is difficult to argue for a shift in ECB policy over the next 6-12 months, provided there are no major geopolitical disruptions.

With growth still slow and inflation broadly at target, there is limited justification for either renewed tightening or rapid additional easing for the time being.