18/02/2026

Net International Investment Position

Newsletter #89 - February 2026

Most investors are, of course, familiar with the current account in the balance of payments, since it is one of the most frequently cited macroeconomic statistics. Far fewer, however, pay attention to the Net International Investment Position (NIIP), even though it is tightly linked to the current account and, over time, largely reflects what persistent surpluses and deficits actually accumulate into.

Current account in the balance of payments

The current account is often treated as shorthand for the trade balance: the balance on goods plus the balance on services. In broad terms, that interpretation is correct, because it discloses whether a country exports more than it imports (or vice versa). Yet this is only one way of reading the current account.

Another, and often more revealing, approach is to look at the current account through a sectoral lens, most notably by separating the public sector and the private sector. At first glance, this may seem odd: governments do not “export” in the same direct way companies do, so why would the public sector matter for the external balance?

It matters because the current account can be expressed, in simplified form, as the sum of the net saving positions of the public and private sectors. Put differently: a country’s external surplus or deficit mirrors whether, on aggregate, domestic sectors are saving more than they invest or investing more than they save.

Current account = Public sector (surplus/deficit) + Private sector (surplus/deficit).

This identity has an important implication for both economic analysis and investment strategy. A country can run a sizable public-sector deficit and still record a current-account surplus, provided that the private sector saves substantially more than the government spends. In such a case, private-sector net saving more than “finances” the fiscal deficit, and the country as a whole remains a net lender to the rest of the world.

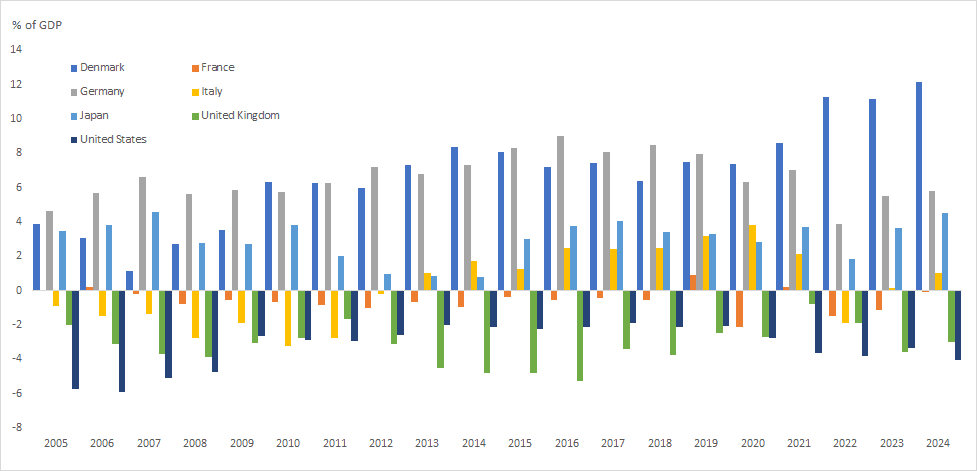

Italy is a useful example. Market narratives often focus on Italy’s public debt dynamics, a concern that is not misplaced. At the same time, Italian private-sector saving has frequently been strong enough to offset public-sector deficits, which is why Italy has recorded a positive current account in most years, as illustrated below in Figure 1.

Figure 1 Current account as percentage of GDP (source OECD)

The most extreme example is Japan. For many years, Japan has combined a large current-account surplus with persistent public-sector deficits that have contributed to a very high level of government debt. The sectoral interpretation helps explain how these seemingly conflicting facts can coexist: sustained private-sector net saving can underpin an external surplus even as the state runs deficits.

By contrast, the United States has run current-account deficits for decades. Over the past ten years in particular, these deficits have been driven predominantly by a large and persistent public-sector deficit, which has outweighed private-sector saving.

This naturally raises the question: if a country runs current-account deficits year after year, what happens to those deficits as they “accumulate” over time?

The short answer is that they show up in the country’s Net International Investment Position (NIIP).

Flow versus stock

It is important to distinguish between the current account and the Net International Investment Position (NIIP), because they describe two different things.

The current account in the balance of payments is a flow: it measures what happens over a period of time (for example, over a quarter or a year).

NIIP is a stock: it measures what exists at a point in time - the net value of a country’s external assets minus its external liabilities.

Everything else being equal, a country that runs a current-account surplus year after year will gradually build up a net external asset position. Over time, that surplus “adds to” the country’s NIIP.

A useful analogy is a company that generates operating profit consistently. If profits are not fully distributed, they accumulate as retained earnings on the balance sheet. In the same way, sustained external surpluses tend to accumulate into a stronger external balance sheet, i.e. a higher NIIP.

Net International Investment Position

Even so, NIIP is not determined solely by the mechanical accumulation of current-account flows. The relationship is complicated by valuation effects.

As the prices of financial assets move, the market value of what a country owns abroad (and what the rest of the world owns in that country) changes as well. In addition, exchange-rate movements can materially affect valuations because external assets and liabilities are often denominated in different currencies. These two channels, asset-price changes and currency swings, can sometimes dominate the flow effect over shorter horizons.

For simplicity, we will assume that the main driver of a country’s NIIP over long periods is the accumulated current-account balance.

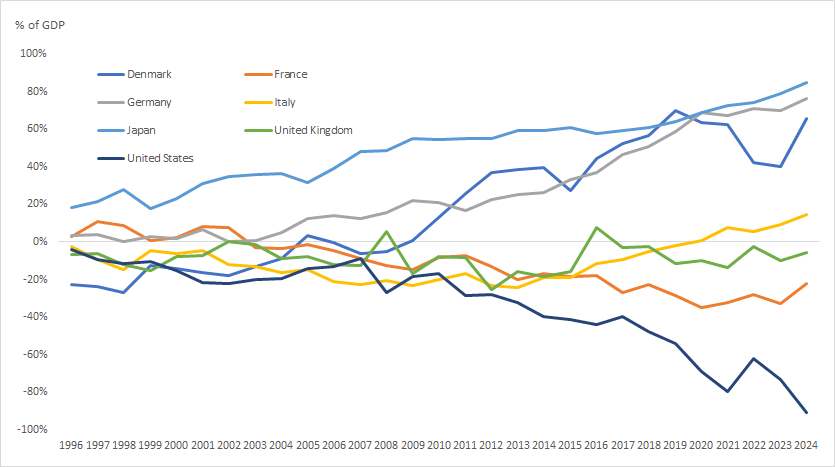

Figure 2 Net International Investment Position (source IMF)

When looking at NIIP, it is hardly surprising that traditional export powerhouses such as Germany and Japan display large positive net positions relative to GDP. Persistent surpluses, sustained over long periods, typically translate into stronger external balance sheets.

Denmark is also notable. It illustrates how sound and consistent economic policies can generate benefits over time, especially in a configuration where both the public and private sectors are in surplus. When that happens, the economy strengthens domestically while also building an improving net position vis-à-vis the rest of the world.

Italy, as discussed earlier, is particularly interesting because it has a positive NIIP. This makes the “run on Italian public debt” narrative less straightforward than it might appear. If the private sector’s net asset position is large, it can act as a stabilizing force: the country’s aggregate balance sheet is not purely a story of public liabilities.

France, by contrast, appears more exposed. We have previously discussed weaknesses in French economic policy, and a negative NIIP makes it easier for markets to put pressure on French government bonds. A net debtor position can amplify confidence shocks, especially when fiscal credibility is questioned.

And the United States

The United States poses the most debated case. How can the US run persistent current-account deficits and end up with an NIIP close to minus 100% of GDP?

This outcome is only feasible because the US dollar plays the role of the world’s dominant reserve and transaction currency. Global investors and institutions have, for decades, been willing to hold large quantities of dollar assets. As a result, the US can finance ongoing current-account deficits by issuing claims to foreigners - most prominently through US equities and US government bonds.

The more interesting question is not whether the US can finance its deficit today, but how long the rest of the world will be willing to finance it on similar terms. If credible alternatives emerge (other currencies, other deep capital markets, other “safe asset” pools) global portfolios could gradually reallocate.

And the uncomfortable, “stupid” answer is that nobody knows the timing in advance. These shifts only become obvious once they are underway - until, suddenly, everyone knows.

Do not get in front of a freight train

It is rarely possible to predict exactly if, when or how quickly a structural regime shift will occur. What is possible, however, is to monitor a small set of indicators that, when they move together, tend to precede large, discontinuous capital reallocations: persistent inflation surprises, credible shifts in central-bank reaction functions, widening rate differentials that compress abruptly and political mandates that materially change fiscal policy.

End of the yen carry trade

For years, the yen carry trade has been a “bread-and-butter” strategy in global markets: borrow cheaply in yen, deploy the proceeds into higher-yielding non-yen assets, and, where risk appetite allows, add leverage to amplify the rate differential.

A potential catalyst for a reversal is a durable change in Japan’s policy mix. Prime Minister Sanae Takaichi’s Liberal Democratic Party has recently secured a very strong mandate in the Lower House, which increases the probability of fiscal expansion through tax measures and higher spending.

If that fiscal stance were to raise underlying inflation pressure, the Bank of Japan could face a less forgiving trade-off and, over time, might be compelled to tolerate higher domestic yields, while still preserving the appearance (and credibility) of institutional independence.

To illustrate the mechanism (not to forecast the numbers), assume the BoJ were to push policy rates materially higher over the next year and long-end JGB yields repriced accordingly; simultaneously, assume the United States moved in the opposite direction as the Federal Reserve approached a leadership transition, with markets pricing in a more accommodative path.

In such a scenario, the logic of the carry trade deteriorates quickly. Once Japanese yields become competitive on a currency-hedged basis, the incentive for Japanese investors to remain in foreign sovereign bonds diminishes and repatriation flows can accelerate. At that point, what looked like a stable, incremental position can unwind in a disorderly way because the trade is crowded, leveraged and mechanically sensitive to volatility.

A regional, rather than global, economy

It is also not unreasonable to argue that globalisation has become more contested, particularly under an “America First” policy posture that encourages allies and partners to re-evaluate economic dependence and strategic exposure.

If the EU, Canada, Japan and South Korea increasingly prioritise domestic and regional investment (defence industrial capacity, energy security, supply-chain redundancy, and critical digital infrastructure, including AI, software and communications) then a portion of the capital that has historically been “parked” in US assets could be redirected. The key point is not ideology; it is portfolio construction under new constraints: resilience, security of supply and political risk management.

In that environment, governments can also create explicit incentives to repatriate capital (tax structures, regulatory preferences, procurement commitments and co-investment vehicles), which, taken together, can gradually tilt the marginal flow away from US markets and toward regional projects

A reserve currency that feels less “risk-free”

Nothing indicates that the world is currently abandoning the US dollar as the dominant reserve currency. But reserve status is not a moral entitlement; it is a financial equilibrium sustained by credibility, deep markets and stable institutions.

History provides a useful warning. Sterling once played an outsized international role, but its global status diminished over time as Britain’s relative economic position eroded and the postwar monetary system increasingly centred on the dollar. The point is not that the dollar is “about to” repeat sterling’s trajectory; the point is that even the leading reserve currency can lose ground if policy credibility and institutional trust are persistently weakened.

Even for a country that issues the world’s primary reserve currency, irresponsible economic policy is only tolerated up to a point, and the market’s tolerance is typically revealed only when it starts to disappear.

Impact of changes

As an investor, it is crucial to monitor shifts in current-account flows and the evolution of the Net International Investment Position (NIIP), because slow-moving imbalances can compound into abrupt market moves once preferences change.

On the current account, the key transmission channel is trade. If the global economy becomes more regionalised (shorter supply chains, more intra-bloc commerce) there is structurally less need for US dollar intermediation in trade settlement and reserves recycling, which can gradually reduce baseline dollar demand.

On the NIIP, the bigger risk is a reallocation of portfolios. If central banks decide to hold fewer dollar assets, the adjustment can be persistent rather than tactical; recent increases in gold purchases over the past 12–24 months illustrate that reserve composition is not fixed. If, in parallel, the private sector rotates away from dollar-heavy assets such as US Treasuries and US equities, the marginal impact on the dollar can become nonlinear.

Consider index structure: US equities are roughly 70% of the MSCI ACWI currently. If that weight were to fall toward 50% or 40%, it would imply large, mechanical outflows from US assets into other regions, currencies and instruments. Such a shift would represent a sizeable re-pricing of the dollar’s “default” allocation within global portfolios.

In that scenario, the US dollar could weaken materially. The magnitude is uncertain, but sustained outflows, especially if paired with continued policy slippage, make a higher EUR/USD exchange rate plausible. A retest of 1.60 in EUR/USD is not the base case, but it is within the realm of outcomes under a genuine, broad-based reallocation away from dollar assets.