24/03/2026

Beyond higher oil prices

Newsletter #90 - March 2026

The weight of energy

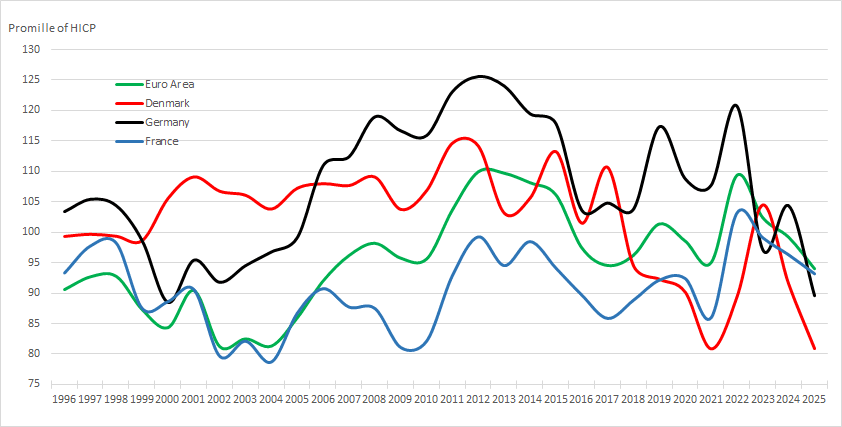

The weight of energy in the Harmonised Index of Consumer Prices (HICP) is not constant over time. Rather, it is revised periodically in order to reflect changes in the relative importance of individual components within the consumption basket.

Moreover, the composition of the consumer basket varies across countries, largely as a consequence of differences in national energy policy and the corresponding energy mix. As illustrated in Figure 1, cross-country variation in the structure of energy supply is closely associated with differences in the weight assigned to energy in national HICP baskets.

Germany constitutes a particularly revealing case. Following the decision taken in the mid-2010s to phase out nuclear power, the country became increasingly dependent on imported natural gas, notably from Russia. This strategic vulnerability became evident in 2022, when the Russian invasion of Ukraine triggered a sharp escalation in gas and oil prices. As a result, the weight of energy in Germany’s HICP increased markedly, exceeding 12 per cent, or 120‰.

At the same time, this composition also generates a symmetrical effect in periods of falling fossil fuel prices. When oil and gas prices decline, the weight of energy in Germany’s HICP tends to decrease comparatively rapidly.

France presents a contrasting case. A substantial part of French energy policy has long been based on nuclear power generation. This has contributed to a significantly more stable energy component in the French HICP, as the country is less directly exposed to fluctuations in international fossil fuel markets.

Denmark, by comparison, occupies a relatively advantageous position. Domestic production of oil and gas covers an important share of national demand, while large-scale wind power generation and access to comparatively inexpensive Swedish electricity further strengthen energy supply conditions. Together, these factors contribute to moderating energy costs for Danish consumers and, by implication, to reducing volatility in the energy component of the HICP.

Figure 1 Weight of energy in HICP for different areas (source Eurostat)

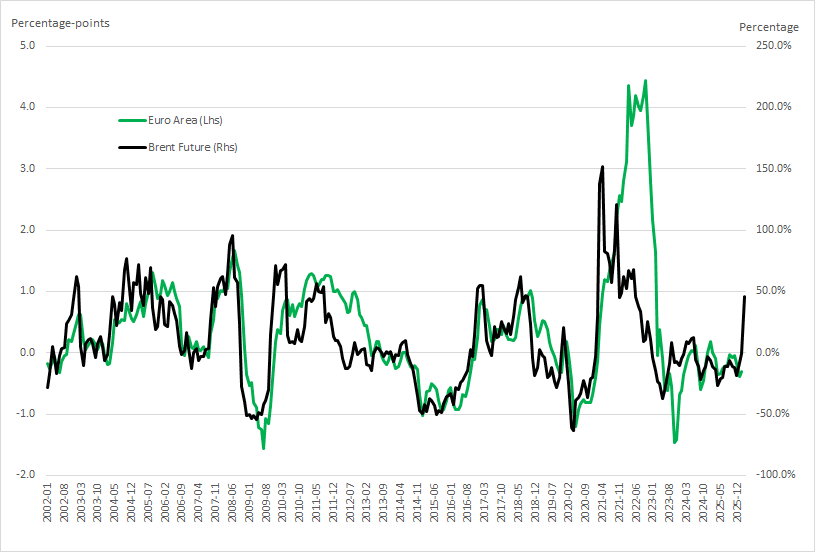

Impact on annual HICP from changes in oil prices

It is important to bear in mind that inflation measures the rate of change in the price index. Consequently, in ordxer to assess the effect of changes in oil prices on the HICP, the relevant variable is the annual rate of change in oil prices rather than the price level itself.

At the same time, differences in price levels remain economically significant. A rise from USD 20 to USD 40 per barrel represents the same percentage increase as a rise from USD 50 to USD 100 per barrel. However, the consumer perception of these two developments is markedly different, since the absolute price level shapes both spending behaviour and inflation expectations.

In Figure 2, the annual change in the price of Brent crude oil (the black line relates to the right-hand side axis) is compared with the contribution of the energy component of the HICP to annual HICP inflation (the green line relates to the left-hand side axis).

Unsurprisingly, the two series display a considerable degree of overlap, indicating a close relationship between oil price developments and energy-driven inflation.

The spike in Brent oil prices to around 150 per cent at the beginning of 2021 does not primarily reflect a fresh oil price shock. Rather, it represents a normalisation following the collapse in oil prices during the COVID-19 pandemic, when Brent crude briefly fell to below USD 20 per barrel in 2020.

Figure 2 Energy's contribution to annual HICP inflation and YoY changes in Brent Futures (source Eurostat and Investing.com

The conflict in Ukraine, which began in February 2022, may provide some indication of the direction in which HICP inflation could move over the subsequent 12 to 24 months, although much depends on the duration of the conflict between the United States, Israel and Iran. It should also be emphasised that the chart considers only developments in oil prices. In 2022, the largest contribution to the surge in energy prices stemmed from the sharp increase in the price of Russian natural gas, on which the European Union was heavily dependent.

In Figure 2, it is assumed that the price of Brent crude will stand at approximately USD 110 per barrel at the end of the month, as indicated by the spike in the most recent observation for Brent futures. This raises the question of what might constitute a reasonable estimate for the contribution of energy to annual HICP inflation in the euro area.

Given that oil prices declined during the spring of 2025, a plausible approximation is that energy could add between 1.0 and 1.5 percentage points to annual inflation in the coming months, provided that historical patterns continue to hold.

Euro area HICP inflation has recently been close to 2 per cent year on year, with energy making a negative contribution of approximately 0.3 percentage points. On this basis, euro area inflation could rise to between 3 and 4 per cent, with the most likely outcome appearing to lie near the upper end of this range.

How the European Central Bank would respond to such an increase in inflation is difficult to determine at the present juncture, not least because uncertainty surrounding developments in the Persian Gulf is greater now than it has been for decades. The longer the conflict persists, the greater the likely impact on inflation and, by extension, on monetary policy.

From Russia to Qatar to…..?

For the European Union, the conflict involving the United States, Israel and Iran may carry major geopolitical and economic implications. Most importantly, it risks underscoring once again the structural fragility associated with Europe’s dependence on external energy suppliers.

At the time of Russia’s invasion of Ukraine, many EU countries remained highly dependent on Russian natural gas. The political response was therefore to accelerate the shift away from Russian supplies and to diversify the Union’s energy imports. A substantial part of this replacement came from liquefied natural gas imported from Qatar and other Persian Gulf producers.

Should LNG transport routes through the Strait of Hormuz become seriously disrupted, the European Union could once again find itself confronted with a pressing supply challenge. Under such circumstances, a central question emerges: which countries are capable of supplying the EU with natural gas in the short-to-medium term, and at what economic and geopolitical cost?

Long-term impact from energy price shocks

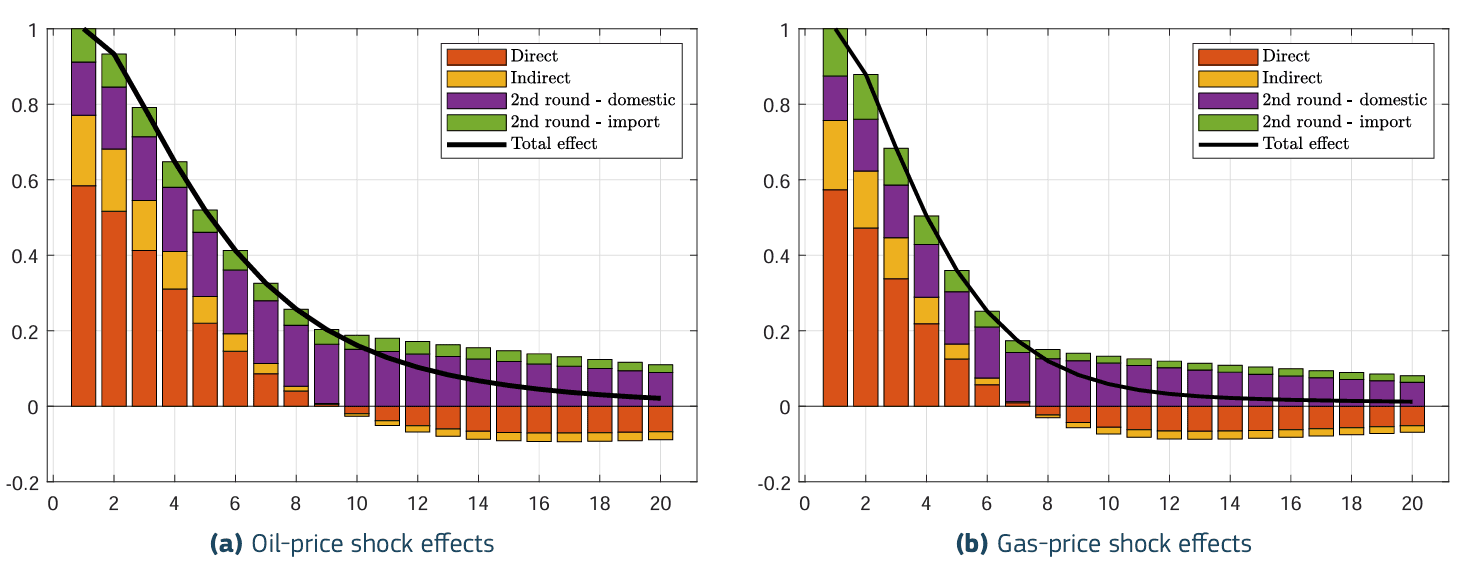

The European Commission’s Directorate-General for Economic and Financial Affairs (DG ECFIN) published an especially interesting Discussion Paper in November 2025, entitled Energy Commodity Price Shocks in the Euro Area (Discussion Paper No. 233).

On the basis of a dynamic stochastic general equilibrium (DSGE) model, the paper estimates the effects of oil and gas price shocks on HICP inflation. One of the principal advantages of a DSGE framework is that it allows for an assessment not only of the direct impact of energy price shocks, but also of the indirect and second-round effects on inflation, as illustrated in Figure 3.

Figure 3 Modelled effects on inflation from energy price shocks (Source EU DG ECFIN)

In the discussion paper the authors conclude that:

“Overall, the decomposition shows that direct effects substantially understate the inflationary impact of commodity price shocks. General-equilibrium channels, via cost pass-through, wages, and other second-round effects, amplify and prolong the initial shock."

Figure 3 shows clearly that the initial price shock accounts for only slightly more than 50 per cent of the total inflationary impact. This direct effect fades relatively quickly, largely disappearing over a period of around two years, or eight quarters, as indicated in the figure.

By contrast, the second-round effects appear to be more persistent and economically more significant in the longer term. This is because they influence underlying behavioural mechanisms in the economy, including wage formation and broader price-setting dynamics.

What lays ahead

If the conflict involving the United States, Israel and Iran were to persist for a prolonged period, there would be a significant risk that major oil and gas installations in and around the Persian Gulf could suffer severe damage. As we write this newsletter, more and more reports are coming in stating that significant damage to oil and gas installations have already happened.

In the medium term, such significant damages could result in substantial disruptions to supply chains, as it can take 2-5 years to bring capacity back to previous levels.

There are already reports suggesting that shortages are beginning to emerge in certain energy-related markets, including jet fuel.

Given the evidence presented in this newsletter, it appears likely that annual inflation in the euro area could rise to between 3 and 4 per cent.

Under such circumstances, any further interest rate cuts by the European Central Bank now appear highly unlikely. Indeed, if the conflict were to continue and the ECB were to conclude that inflationary pressures were spreading more broadly through the economy, as discussed earlier, it could even consider renewed interest rate increases.

If the yield curve steepens due to the fear for sustained inflation pressure, this could force the ECB to increase interest rates. Such rate hikes would raise the risk of recession in the euro area, where private consumption and investments in real terms will fall significantly.

The ECB therefore faces the difficult task of striking a very delicate balance in its monetary policy during the remainder of 2026.