17/04/2026

On blockades, supply and prices

Newsletter #91 - April 2026

Prices are one thing - supply another

Much of the current anxiety in global energy markets is centred on high oil prices and the broader rise in energy costs. Yet the more important issue may soon be supply rather than price.

So far, limited attention has been paid to the physical flow of oil. That may change rapidly. Iran and the United States now appear to have created a “double” blockade in the Strait of Hormuz, raising the risk of a prolonged disruption to crude and refined product shipments.

For now, nobody can say with confidence how long this situation will last. But if the disruption continues, the consequences for global supply chains could become severe. This applies not only to crude oil, but also to refined products such as petrol, diesel, jet fuel and kerosene.

A Reuters article published on 14 April 2026 cites IEA estimates suggesting that shortages of jet fuel and kerosene could emerge by June. The Gulf states export close to 400,000 barrels per day of jet fuel and kerosene, and almost 375,000 barrels of that volume goes to Europe.

That shifts the focus. The key question is no longer simply how high prices can rise, but whether supply can be replaced at all.

Can Europe replace 75% of its daily jet fuel and kerosene imports from sources outside the Gulf states? In the short term, that looks unlikely. Reuters reports that the IEA estimates that if only half of the disrupted supply can be replaced, Europe could face shortages during June.

In other words, this is becoming less a story about price pressure and more a story about physical scarcity. Markets can adapt to higher prices. They adapt far less easily to missing barrels.

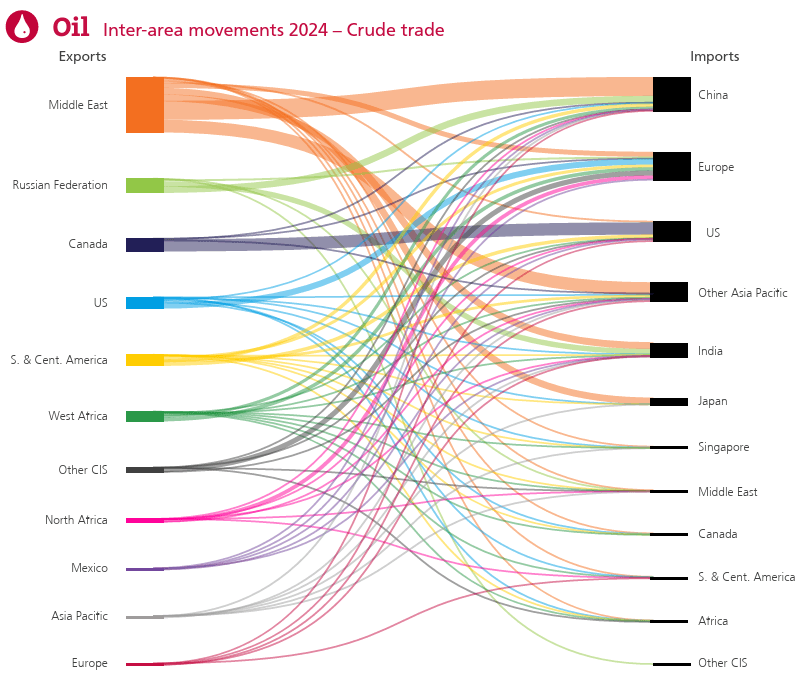

Flow of crude oil

To understand the supply implications of a “double” blockade of the Strait of Hormuz, one must look carefully at the structure of global oil flows. Prices tend to attract the most immediate attention, but in a prolonged disruption the more important issue is physical supply. The figures below help illustrate that distinction.

Figure 1 Crude Oil Export and Import 2024 (source; Energy institute)

On the left side of the chart are the world’s main crude oil exporting regions and countries. On the right side are the principal importing regions and countries. The connecting streams show the direction and relative scale of the trade flows.

Canada offers a useful example. It is a major exporter of crude oil, and by far the largest share of its exports goes to the United States, represented by the broadest dark purple stream. Smaller shares are exported to China, Other Asia Pacific and Europe. The point is straightforward: crude oil does not move evenly across the world. It moves through established trade routes shaped by geography, infrastructure and long-standing commercial relationships.

That becomes highly relevant when assessing the consequences of a disruption in the Strait of Hormuz.

Impact of the “double” blockade

The Middle East remains the world’s largest crude oil exporting region, accounting for roughly 40% of global crude oil exports. That alone makes any blockade in the Strait of Hormuz a matter of global importance.

Most Middle Eastern crude exports go to Asia. China receives around 35% of the region’s crude exports, India 13%, Japan 12% and Other Asia Pacific 23%. This suggests that the greatest immediate crude oil vulnerability lies in Asia rather than in Europe. For these economies, replacing Middle Eastern crude at short notice would be difficult, costly and logistically complex.

Europe is less exposed on the crude side. It imports only 8.8% of Middle Eastern crude exports. That does not mean Europe would avoid the effects of disruption, since oil prices are set in a global market. It does mean, however, that Europe’s direct dependence on Middle Eastern crude is materially lower than that of the major Asian importers.

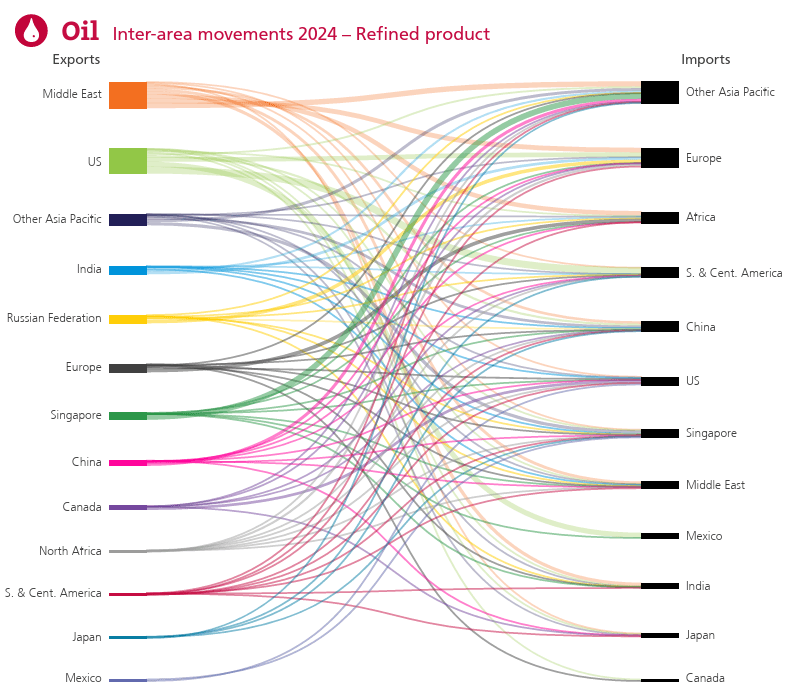

Flow of refined products

The picture changes when the focus shifts from crude oil to refined products.

Figure 2 Refined product Export and Import 2024 (source; Energy institute)

Refined products matter because they are the fuels that economies use directly: petrol, diesel, jet fuel and kerosene. A disruption here can therefore create more immediate shortages than a disruption in crude alone.

For refined products, Europe receives around 18% of its imports from the Middle East, while Other Asia Pacific receives around 20%. In other words, both regions may need to replace roughly one fifth of their refined product imports from alternative suppliers. In the case of jet fuel and kerosene, the challenge may be even larger. As Reuters has reported, as much as 75% of disrupted supply may need to be replaced.

That is where the supply risk becomes significantly more serious. Replacing such volumes is not just a matter of paying a higher price. Refining systems are complex, shipping capacity is limited, and alternative suppliers may not have enough spare export capacity available at short notice.

Countries such as China, Singapore and Japan do have substantial refining capacity. But that does not resolve the problem. As noted earlier, crude oil itself may also be difficult to secure if flows from the Middle East are disrupted. Refining capacity is only valuable when there is sufficient feedstock to run through it. If the crude is not available, additional refining capacity offers little relief, regardless of how advanced or extensive that infrastructure may be.

The broader conclusion is therefore clear. If the “double” blockade of the Strait of Hormuz proves short-lived, the main consequence may be another spike in energy prices. But if it continues for longer, supply will become the more serious concern.

Markets can adjust to high prices. They adjust much less easily to missing barrels and unavailable fuel.