18/05/2026

The Canary In The Coal Mine

Newsletter #92 - May 2026

What triggers major dislocations in the financial markets?

Identifying the precise catalyst for a major market dislocation is, of course, the analytical equivalent of the Holy Grail: whoever could do so with consistent accuracy would accumulate extraordinary wealth in short order. Since no such certainty exists, the more productive exercise is to monitor the segments of the financial system that are structurally most vulnerable, and therefore most likely to serve as the initial point of fracture — the canary in the coal mine.

At present, equity markets appear remarkably resilient, dismissing geopolitical conflicts, pandemic aftershocks and persistent inflationary pressures alike. The prevailing consensus holds that every correction represents a buying opportunity, and that secular growth in artificial intelligence, semiconductor infrastructure and hyperscaler capital expenditure will indefinitely underwrite elevated valuations.

However, fundamentals tend to reassert themselves with considerable force. Our assessment is that the United Kingdom’s sovereign Gilt market currently represents one of the most structurally precarious fixed-income markets among developed economies, and therefore warrants close monitoring as a potential systemic flashpoint.

The United Kingdom: deteriorating fundamentals

The United Kingdom’s economic and fiscal position has deteriorated materially since its departure from the European Union. Growth has, at best, been anaemic, consistently lagging behind the EU average, and this prolonged underperformance has inflicted considerable damage to the public finances.

On the political front, the situation is equally unsettled. Reform UK under Nigel Farage achieved substantial gains in the local elections held at the beginning of May, signalling a pronounced erosion of support for the governing Labour Party.

In Wales, the results were particularly damaging for Labour, which secured a mere 11.1% of the vote and nine seats. Reform UK obtained 34 seats, while the overall winner, Plaid Cymru, captured 43 of the 96 available seats in the Welsh Parliament.

Notwithstanding Labour’s absolute majority in Parliament, the party is mired in an internal dispute over whether Prime Minister Sir Keir Starmer should remain in office, with several ministerial resignations already recorded. This type of political instability is precisely the environment in which sovereign bond markets become acutely sensitive to adverse developments.

Such conditions are anathema to bond markets, which historically react to fiscal uncertainty and political dysfunction with rapid and sometimes disorderly yield adjustments.

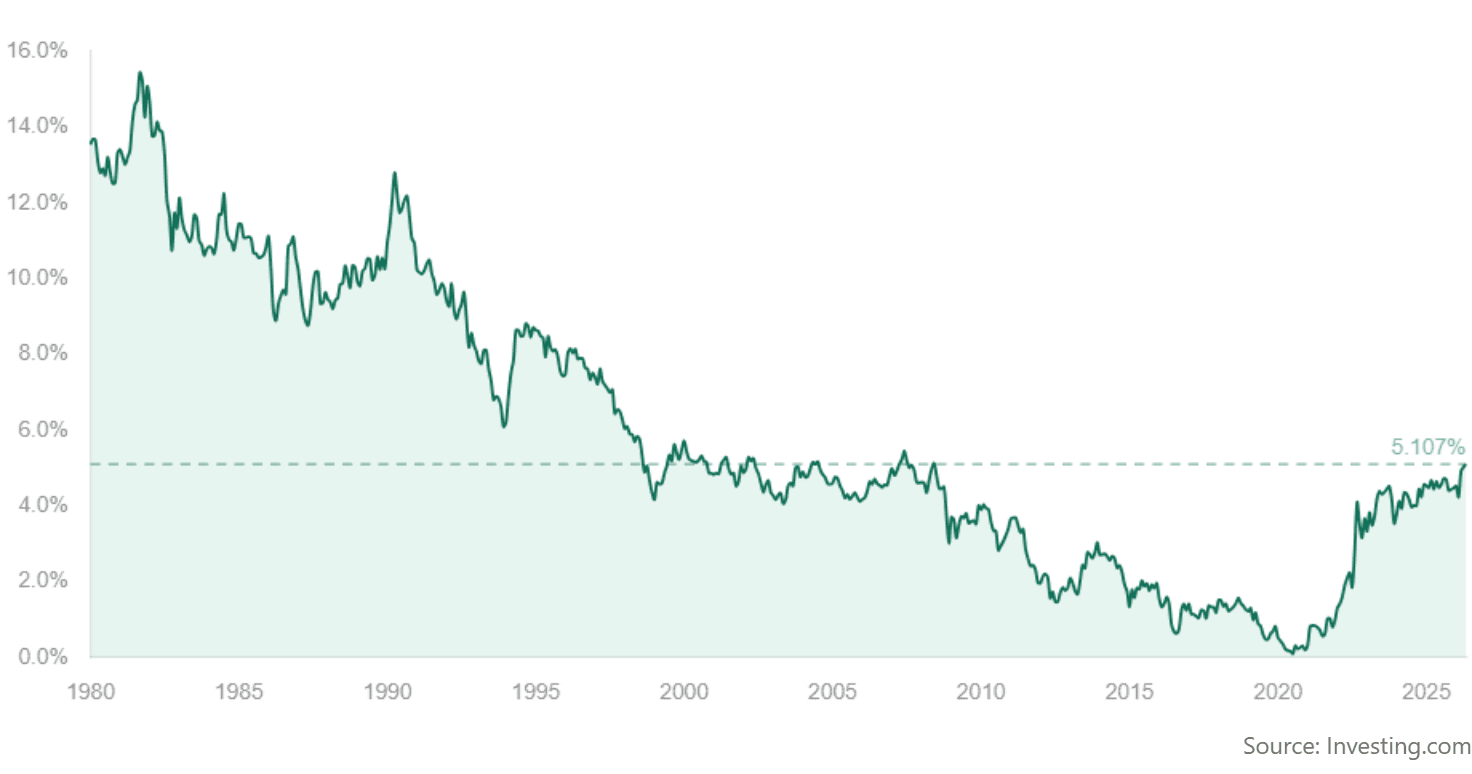

UK 10-year Gilts are currently trading at yields that exceed those recorded during the tenure of Prime Minister Liz Truss, whose 48-day administration triggered the last Gilt market crisis in 2022, see Figure 1.

This is a significant concern, given that the UK is already operating with a fiscal deficit of approximately 5% of GDP (and that figure does not yet incorporate the substantial additional expenditure required to raise defence spending to the NATO target range of 3.0–3.5% of GDP).

Figure 1 UK 10-year GILTS yield (source; Investing.com)

The central question for investors is whether the conditions are in place for a sustained, disorderly sell-off in the Gilt market.

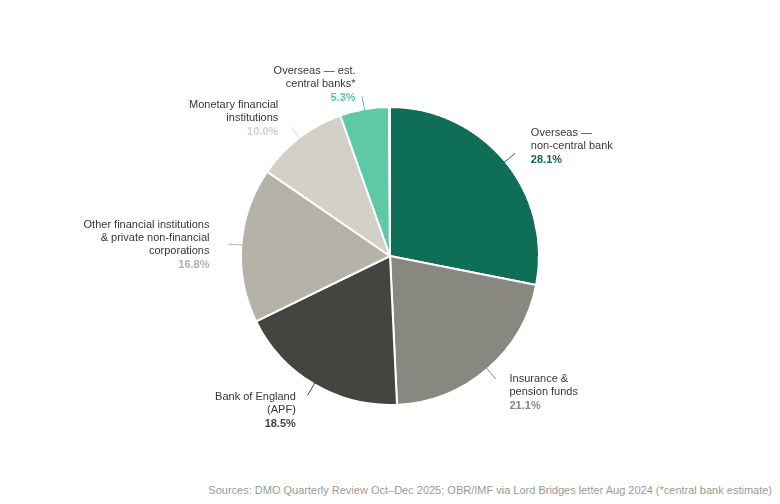

As illustrated in Figure 2 below, the Gilt ownership structure does not offer meaningful reassurance. The predominant holders are not central banks aligned with the Bank of England’s stabilisation objectives.

Available estimates suggest that the Bank of England and other sympathetic central banks collectively hold no more than 25% of the outstanding stock of Gilts.

Domestic pension funds, once a natural and stabilising buyer of long-dated Gilts, suffered severe stress during the 2022 episode, when the rapid increase in yields triggered liability-driven investment (LDI) unwinds. Their capacity to absorb additional issuance or provide a meaningful price-floor in a renewed sell-off is therefore severely constrained.

A substantial proportion of overseas holdings are attributable to Irish- and Luxembourg-domiciled investment funds, along with other financial institutions and private non-financial corporations — all of which are categorised as “fast money” that can be redeemed or repositioned at very short notice.

Figure 2 Holdings of UK GILTS by sector at the end of Q3 2025

With a current account deficit of approximately 4%, a fiscal deficit of 5.1%, and a debt-to-GDP ratio exceeding 131%, the United Kingdom presents a compelling candidate for a disorderly sovereign bond market event, particularly given that more than 50% of outstanding Gilts are held by “fast money” investors whose mandates permit redemption at short notice.

The broader macroeconomic context

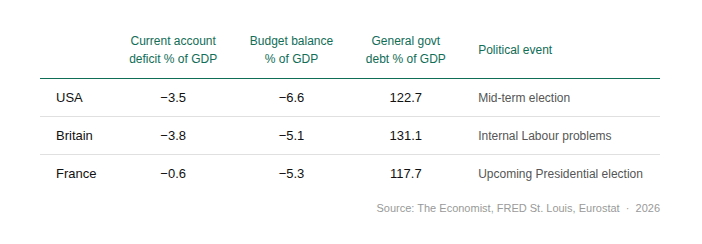

The United Kingdom is far from alone in its fiscal predicament. The United States and France are confronting comparably unsustainable structural imbalances, as reflected in the key metrics summarised in Table 1, below.

Across all three economies, the underlying fiscal and external balances have deteriorated to levels that, historically, have preceded significant market stress events.

Table 1 Current account, budget, debt and coming events

The question we pose to investors is whether a disorderly collapse in the UK Gilt market could function as a systemic catalyst comparable to the failure of Bear Stearns in 2008, an event that crystallised what had until then been a contained subprime stress into a full-blown global financial crisis. That outcome cannot be dismissed.

We will continue to monitor the Gilt market closely. In our assessment, it remains a credible candidate for the role of canary in the coal mine.

Is the US far behind the UK?

In the week of Ascension, the US Bureau of Labor Statistics released both CPI and PPI figures for April, painting a concerning picture for the domestic inflation outlook.

Producer prices rose 1.4% in April on a seasonally adjusted basis, translating into a year-on-year increase of 6% — a level not seen since the inflationary surge of 2022. Consumer prices equally continued their upward trajectory, with year-on-year CPI climbing 3.8% in line with market expectations. Gasoline prices at the pump have surged 28.4% over the past twelve months, adding further strain to household budgets.

Meanwhile, capital markets are adjusting to the new inflationary reality. Ten-year US Treasuries are now trading at yields exceeding 4.5%, reflecting mounting investor concerns over the persistence of price pressures. Most notably, the US Treasury issued a 30-year bond carrying a coupon of 5%, the first such issuance at that level since 2007.

The parallels with the UK are becoming harder to dismiss. With a widening budget deficit, a debt-to-GDP ratio that leaves little room for manoeuvre and midterm elections constraining any serious appetite for fiscal consolidation, the US finds itself increasingly caught in the same bind that has defined the UK's economic predicament.

Investors should be following these developments closely in the months ahead.